Modern payment stacks are under pressure: faster settlement expectations, stricter compliance, and a constant stream of fraud attempts. That’s where AI in payment processing becomes more than a buzzword; it’s the engine behind speed, accuracy, and intelligent automation across authorization, routing, monitoring, reconciliation, and dispute handling.

Instead of waiting on manual checks or one-size-fits-all rules, organizations can use AI to interpret transaction context in real time and make decisions with far fewer delays. The result is a better customer experience, fewer operational headaches, and a system that improves as it learns from new patterns.

In this blog, we’ll explore how AI is transforming payment processing by improving speed, accuracy, and scalability, along with key use cases and practical insights for businesses.

What is AI in Payment Processing?

AI-powered payment systems use machine learning and related techniques to interpret transaction data beyond static validation rules. In other words, instead of treating each payment like a form submission, AI treats it like an event with context: who initiated it, what changed, where it came from, how it compares to historical patterns, and whether it matches known risk behaviors.

That’s the key difference between rule-based systems and AI-driven processing. Rules are deterministic if/then logic that works well for known scenarios. AI-driven processing can generalize from data, detect subtle anomalies, and adapt when criminals change tactics. In practice, many teams combine both, using rules for guardrails and AI for adaptive decisioning.

Core capabilities typically include:

AI Payment Processing Capabilities Explained

- Real-time transaction analysis (risk and quality checks during authorization).

- Intelligent routing of payments to reduce time-to-settlement and avoid costly paths.

- Fraud detection and prevention using behavioral and pattern-based signals.

- Automation of payment workflows (approvals, holds, exceptions, and downstream actions).

When you implement this properly, AI in payment processing becomes a decision layer, not an afterthought, helping teams reduce both operational delay and fraud losses.

Limitations of Traditional Payment Processing

Traditional payment workflows were built for reliability under manageable volume, not for the modern reality of high-velocity digital commerce. As transactions scale, the bottlenecks become more expensive and more visible.

- Delays in transaction processing: authorization and settlement can stall while systems wait for upstream validation or offline risk checks.

- Manual intervention in exception handling: when rules trigger holds, analysts often need to review evidence and decide outcomes case-by-case.

- High error rates in reconciliation: matching transactions across systems (gateway, processor, core banking, accounting) can become messy, especially when fields vary by source.

- Limited fraud detection capabilities: static rules are vulnerable to adversaries who probe boundaries and adapt slowly.

- Scalability challenges: more volume means more exceptions, more queues, and more costs to maintain service levels.

- Poor user experience due to latency: if customers experience delays at checkout, conversion rates usually suffer.

Even the best teams feel the strain: operations teams get stuck in repetitive investigations, product teams get blamed for latency, and finance teams inherit reconciliation chaos. AI in payment processing addresses these pain points by turning raw payment data into actionable decisions faster than humans can process exceptions.

How AI is Transforming Payment Processing

The real transformation isn’t just that AI can “detect fraud.” It’s that it can optimize the full lifecycle of a payment: from intake and validation to routing, authorization decisions, post-transaction monitoring, reconciliation, and dispute workflows.

Here’s what changes when AI moves from a tool to a workflow:

- Automation of end-to-end payment workflows: reduce manual handoffs and accelerate straight-through processing.

- Real-time data processing and validation: validate with richer context (device signals, history, merchant behavior, and geolocation consistency).

- Intelligent decision-making for transaction approvals: approve, step-up authentication, or flag based on risk scores not just thresholds.

- Continuous learning from transaction patterns: models refresh as new fraud campaigns appear and normal behavior evolves.

- Automated reconciliation: match, categorize, and reconcile payment events using probabilistic logic and pattern-based matching.

Key AI functions often include:

- Pattern recognition in transactions (merchant/customer/device/behavior signatures).

- Anomaly detection (unexpected deviations from a customer or merchant’s baseline).

- Predictive analytics for risk scoring (likelihood of chargeback/dispute, account takeover attempts, or mule behavior).

- Automated reconciliation (cross-system mapping and exception explanations).

When executed well, ai in payment processing makes the payment system proactive. Instead of reacting after the fact, teams can prevent issues earlier and route workload where human judgment truly matters.

Key Use Cases of AI in Payment Processing

AI creates value when it’s applied to repeatable, high-impact workflows. The following use cases are common starting points because they connect directly to measurable outcomes: fewer fraud losses, lower operational costs, and faster settlement.

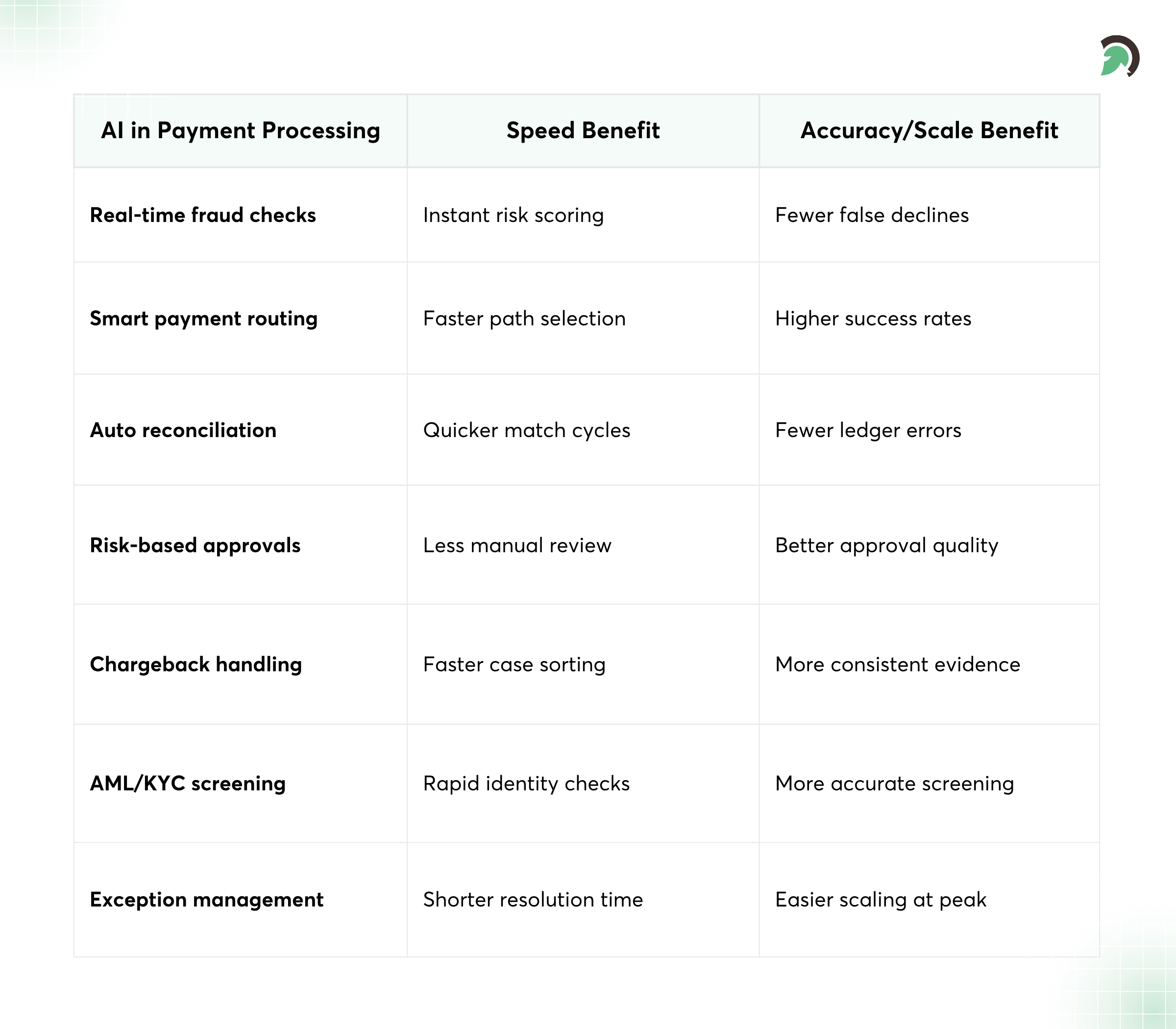

1. Real-Time Fraud Detection

AI monitors transactions in real time and evaluates risk signals through behavioral analysis. Instead of relying only on static rules, it can detect patterns like unusual purchase velocity, inconsistent device behavior, atypical geographic movement, or changes in beneficiary details.

Outcomes:

- Suspicious activities get identified during authorization, not days later.

- Step-up verification can be triggered only when needed, reducing false declines.

2. Intelligent Payment Routing

Payment routing determines which network, acquiring partner, or payment rail processes a transaction. AI can select the optimal path based on performance history, reliability, fees, and success rates.

Outcomes:

- Reduce processing time and transaction costs.

- Improve authorization rates by learning which rails work best for specific contexts.

3. Automated Payment Reconciliation

Reconciliation is where finance teams often spend the most time, especially when transactions have multiple identifiers and slight formatting differences between systems. AI can match payments across systems automatically using probabilistic matching and context rules.

Outcomes:

- Fewer manual accounting hours and fewer missed exceptions.

- Faster period-end closes due to continuous system reconciliation.

4. Risk-Based Transaction Approval

Instead of treating every payment the same, AI dynamically assigns risk scores. Higher-risk transactions can be held, challenged, or routed to additional verification steps. Lower-risk payments can flow through quickly.

Outcomes:

- Better balance between fraud prevention and customer conversion.

- Risk decisions become measurable and easier to refine over time.

5. Chargeback and Dispute Management

Chargebacks are costly not only financially, but operationally. AI can identify dispute patterns early like merchants with rising dispute rates, transactions with evidence gaps, or customers showing behavior consistent with repeated disputes.

Outcomes:

- Automated resolution workflows that help teams respond faster.

- Evidence packaging becomes more consistent, improving dispute win rates.

These use cases are also a practical path to adoption: start where the data is rich, the workflow is repeatable, and the ROI is visible.

How AI Boosts Speed and Accuracy

Technologies Powering AI in Payment Systems

AI in payments is built on a stack of proven technologies. You don’t need “one magical model”; you need a system that can ingest data, learn from it, and integrate safely into payment workflows.

-

Machine Learning (ML)

ML powers risk scoring, anomaly detection, and predictive models for approval and dispute likelihood. Common approaches include supervised learning (trained on labeled outcomes) and unsupervised learning (detecting deviations without explicit labels).

-

Natural Language Processing (NLP) for dispute handling

Disputes often involve narratives, customer descriptions, merchant evidence notes, and support ticket text. NLP can summarize, categorize, and extract structured fields to speed up response workflows.

-

Big Data Analytics

Payment data is high-volume and multi-dimensional. Big data analytics helps unify signals across channels, merchant history, customer behavior, device patterns, network outcomes, and time-based trends.

-

Robotic Process Automation (RPA)

RPA can automate “workflow glue,” moving data, triggering tickets, creating reconciliation entries, and updating internal systems. It pairs especially well with AI because it handles deterministic steps while AI handles probabilistic decision-making.

-

Cloud computing for scalability

Cloud infrastructure supports bursty payment traffic, high availability requirements, and scalable model inference. It also simplifies deployment and versioning.

-

API-based payment integrations

Most teams use APIs to connect gateways, processors, KYC/AML systems, and core banking services. This is essential for real-time checks and fast workflow automation, especially when you’re offering customer-facing services.

At the center, AI in payment processing relies on how these components work together: ingestion, feature engineering, inference, feedback loops, and operational monitoring.

Benefits of AI in Payment Processing

AI delivers value when it changes both system behavior and operational outcomes. That’s why teams measure not just model accuracy, but also transaction success rate, time-to-resolution, fraud loss reduction, and cost per transaction.

Here are the most common benefits organizations pursue through AI payment processing solutions:

- Faster transaction processing speeds: Real-time analysis reduces waiting time and minimizes manual exception queues. With better routing and quicker decisioning, you can improve authorization and settlement performance under load.

- Improved accuracy and reduced errors: AI helps reduce false positives and false negatives by using context and learned patterns. Automated reconciliation also reduces mismatches and repetitive corrections.

- Enhanced fraud detection and prevention: Behavioral anomaly detection can identify fraud attempts that static rules miss. That means fewer “unknown” attacks slipping through and less reactive firefighting.

- Reduced operational costs: Automation lowers the workload for compliance analysts, fraud investigators, and finance teams. Even small efficiency gains across thousands of transactions quickly add up.

- Real-time decision-making capabilities: Approvals, holds, and step-up verification can be driven by risk signals within milliseconds, improving conversion and reducing customer frustration.

- Scalable infrastructure for high transaction volumes: AI systems, especially those deployed in cloud environments, scale more smoothly as traffic grows, without requiring linear increases in headcount.

How AI Enhances Payment Operations

Ultimately, AI in payment processing helps teams align performance, security, and experience without trading one off for another.

Implementation of AI in Payment Processing

Implementation is where most projects succeed or quietly fail. A strong plan avoids “model-first” thinking and instead focuses on workflows, data quality, and safe integration. Below is a practical step-by-step approach that teams use to deploy reliably.

Step-by-step:

- Identify key payment workflows to automate

- Collect and integrate transaction data (including historical outcomes, device signals, network results, and reconciliation fields)

- Select AI models and tools

- Integrate with payment gateways and systems using reliable interfaces and operational controls

- Test for performance, accuracy, and security with realistic traffic and edge-case datasets

- Deploy and monitor in real-time so you can detect drift, anomalies, and unexpected behavior

- Continuously optimize AI models through feedback loops and periodic retraining

How this looks in real projects:

- Start with a measurable target, such as reducing fraud losses by a defined percentage or reducing reconciliation exceptions by a specific number.

- Plan for financial data integration early so models can connect authorization outcomes to settlement and accounting events.

- If your environment requires modern rails and multiple partners, partner with teams that can deliver payment gateway integration services.

For engineering teams, implementation often expands into broader product work like payment processing software development and digital payment software development especially when you’re building customer-facing experiences that depend on low-latency decisions.

Where partners and delivery teams help most:

- Architectural design for safe inference in production

- Feature engineering and data pipelines

- Governance, audit logs, and explainability tooling

- Workflow automation, including fraud monitoring workflow integration

- End-to-end ai integration services to connect models to APIs and internal systems

One practical tip: include an internal documentation plan and cross-team training. When operations and engineering share the same understanding of risk signals, the system improves faster.

Security and Compliance Considerations

AI can only be trusted when security and compliance are treated as first-class requirements. In payments, that means designing for confidentiality, integrity, availability, and auditability, then proving it continuously.

Key considerations:

-

PCI DSS compliance

Keep card data handling scoped correctly. Tokenization, segmentation, and secure transmission patterns help reduce exposure. Even if AI doesn’t “need” raw card data, your system design must still follow PCI requirements.

-

Data encryption and tokenization

Encrypt data in transit and at rest. Tokenize sensitive values where possible. Then limit model access to only the data required for decisioning.

-

Fraud prevention regulations

Follow applicable fraud-prevention and consumer-protection rules, including proper handling of flagged transactions and customer communication requirements.

-

AML and transaction monitoring requirements

AI can enhance monitoring, but it must be aligned with AML requirements and your compliance team’s processes. Many organizations implement components alongside KYC AML automation software to streamline watchlist checks, alerts, and evidence capture.

-

Auditability and transparency in AI decisions

Regulators and internal teams often need to understand why a decision was made. That means retaining decision metadata, logging features used, and enabling explainable outputs where possible.

Challenges of AI in Payment Processing

AI doesn’t eliminate complexity it changes where complexity lives. If teams anticipate the hard parts upfront, they avoid costly rework and stalled rollouts.

Common challenges:

- Data privacy and security concerns: Payment data is sensitive. You need strict access controls, secure pipelines, and careful handling of personal data to prevent leaks and misuse.

- Integration with legacy payment systems: Many institutions rely on legacy processors and older reconciliation tools. Bridging these systems requires careful mapping, reliable APIs, and fallback paths to avoid breaking critical flows.

- Model accuracy and bias issues: Models can underperform when data shifts or behave unexpectedly when trained on biased datasets. Bias mitigation and performance monitoring should be part of the deployment plan not a post-launch activity.

- High implementation costs: Costs aren’t just model licensing. Budget for data engineering, integration, monitoring, security controls, and ongoing retraining cycles.

- Regulatory uncertainty: Different regions may interpret AI governance differently. Teams need early involvement from compliance so implementation choices won’t become roadblocks later.

- Need for continuous monitoring and updates: Fraud patterns change. Customer behavior changes. Systems drift. Continuous monitoring and scheduled updates are necessary to maintain performance.

From a delivery standpoint, successful projects often blend fintech software development expertise with compliance and platform engineering because payments are where correctness matters.

Best Practices for AI-Driven Payment Systems

Best practices keep AI dependable in production. Think of them as the guardrails that protect speed and accuracy while maintaining compliance.

-

Use a secure and compliant infrastructure

Deploy in an environment designed for least-privilege access, encrypted storage, and controlled model inference.

-

Combine AI with rule-based controls

Use AI to make adaptive decisions and rules for deterministic safety checks (such as mandatory fields, known-impossible transactions, or network limits).

-

Maintain real-time monitoring systems

Monitor model outputs, latency, error rates, and drift. Create alerting thresholds and runbooks for incident response.

-

Regularly update and retrain AI models

Fraud evolves. Retraining schedules should reflect transaction seasonality and changes in fraud campaigns.

-

Ensure explainability of AI decisions

Provide evidence for holds and flags. Even if full explainability isn’t possible, provide actionable summaries and decision metadata.

-

Implement strong data governance

Define data ownership, data quality checks, retention periods, and audit trails. This reduces risk and improves model performance.

If you’re creating internal documentation, consider linking to your security playbooks, model monitoring dashboard guides, and compliance SOPs so every team knows where truth lives.

How Businesses Can Get Started

If you’re exploring ai in payment processing and wondering where to begin, you don’t need to build everything at once. You need a sequence that proves value quickly, then expands responsibly.

1. Assess current payment processing challenges

Identify where delays happen (authorization bottlenecks), where errors accumulate (reconciliation), and where losses show up (fraud and chargebacks). Look for measurable pain points, not just “we feel slow.”

2. Identify areas for automation and optimization

3. Choose the right AI technologies and partners

Depending on your stack, you may need support across data pipelines, security architecture, and integration. This is where fintech app development teams often add speed, and where fintech software development partners help reduce integration risk.

4. Start with pilot projects (fraud detection, routing)

Pilots work best when they have a tight scope and a clear success metric, such as reducing confirmed fraud rates or improving authorization success in specific merchant segments. Make sure you also test latency and operational load.

5. Scale with advanced AI capabilities

Once your pilot proves its reliability, expand to additional workflows, such as automated reconciliation and dispute management. If you’re building new payment experiences, align this plan with fintech app development roadmaps to keep the user journey fast and consistent.

Conclusion

AI in payment processing is reshaping how financial systems operate by combining speed, precision, and scalability into a single intelligent layer. From real-time fraud detection to automated reconciliation and smarter routing, businesses can reduce delays, improve accuracy, and handle growing transaction volumes with confidence.

As payment ecosystems continue to evolve, organizations that adopt AI-driven workflows will be better positioned to respond to risk, optimize performance, and deliver seamless customer experiences. The impact goes beyond operational efficiency, supporting long-term resilience and adaptability. As a fintech solutions provider company, EvinceDev helps businesses modernize payment infrastructure with tailored AI solutions designed for agility, security, and future-ready growth.