Key Takeaways

- AI Is Reshaping Banking: AI is helping banks and fintech companies deliver faster, smarter, and more personalized financial experiences.

- Fraud Detection Is Getting Smarter: AI can identify unusual transactions, suspicious login behavior, and potential fraud risks in real time.

- Customer Experience Is Becoming More Personalized: AI-powered banking helps customers get relevant support, product suggestions, spending insights, and financial guidance.

- Automation Is Improving Banking Operations: AI reduces repetitive manual work across document processing, compliance, reporting, and back-office workflows.

- Responsible AI Builds Trust: Banks need strong governance, human oversight, data security, and explainable AI to use automation safely.

Banking is no longer just about transactions. It is about speed, trust, personalization, and making financial decisions easier for customers.

Think about how people use banking today. They want instant answers, faster loan approvals, real-time fraud protection, personalized financial guidance, and secure digital experiences that work without friction. Waiting in long queues, repeating the same issue to support teams, or going through slow manual processes no longer feels acceptable.

This is where AI in Banking is becoming a major force.

Artificial intelligence is helping banks, fintech companies, and financial institutions move from reactive service to smarter, more proactive financial experiences. It is improving customer support, detecting fraud faster, automating repetitive operations, supporting compliance teams, strengthening risk management, and helping financial institutions make better use of data.

But the real value of AI is not just automation. It is the ability to make banking more intelligent, secure, and customer-focused while still keeping human oversight, governance, and trust at the center.

In this blog, we will explore what AI in Banking means, how it is helping banks and fintech companies, its key use cases, benefits, challenges, adoption roadmap, and what financial institutions need to do to use AI responsibly and effectively.

What Is AI in Banking?

AI in Banking refers to the use of artificial intelligence technologies to improve banking operations, customer experiences, risk management, and financial decision-making.

In simple words, AI helps banking systems learn from data, identify patterns, make predictions, automate repetitive tasks, and support better decisions. Instead of relying only on fixed rules or manual processes, banks can use AI to understand customer behavior, detect suspicious activity, analyze financial documents, and respond to customer needs more efficiently.

Some of the main technologies used in this space include:

- Machine learning: Helps systems learn from past data and improve over time.

- Natural language processing: Helps AI understand and respond to human language, which is useful for chatbots, voice assistants, and document review.

- Predictive analytics: Helps banks forecast risks, customer behavior, loan defaults, and market trends.

- Generative AI: Helps create content, summarize reports, explain financial terms, and support customer service teams.

- Computer vision: Helps analyze documents, IDs, checks, signatures, and images.

- AI agents: Help complete multi-step tasks, such as filing a dispute, preparing a report, or guiding a customer through a financial process.

Unlike earlier banking automation, AI in Banking is more adaptive. It can learn from data, improve responses, and help financial institutions make smarter decisions at scale.

Quick Stat:

According to Deloitte, 86% of financial services AI adopters say AI will be very or critically important to their business success in the next two years. This shows that AI is no longer just a technology experiment in banking. It is becoming a core part of how financial institutions plan to compete, serve customers, and operate more efficiently.

Why AI in Banking Is Becoming So Important

The banking and fintech industry is under pressure from multiple directions. Customers expect faster service, fraud risks are increasing, regulations are becoming more complex, and digital-first fintech companies are changing how people interact with financial products.

Traditional banking systems were not always built for this speed and complexity. Many banks still depend on manual reviews, disconnected systems, legacy software, and slow internal processes. AI can help solve many of these problems.

Here are a few reasons why artificial intelligence in banking is becoming so important:

- Customers expect instant service. People want quick answers, real-time updates, and smooth digital experiences.

- Fraud is becoming more advanced. Scammers are using new tools, fake identities, deepfakes, and social engineering tactics.

- Banks need to reduce operational costs. Manual processes take time, increase costs, and create delays.

- Compliance work is growing. Financial institutions must follow strict rules around privacy, lending, fraud, identity checks, and reporting.

- Personalization is now expected. Customers want financial products and advice that match their actual needs.

- Fintech competition is increasing. Digital-first companies are offering faster, simpler, and more flexible financial products.

This is why AI in financial services is becoming more than a technology trend. It is becoming a business necessity.

How AI in Banking Is Helping Banks and Fintech Companies

The biggest value of AI comes from how it solves real problems. It is not only about automation. It is about helping financial institutions become faster, safer, smarter, and more customer-focused.

Below are the most important ways AI is helping banks and fintech companies.

1. AI Is Improving Customer Support

Customer support is one of the most visible areas where AI is making an impact.

Earlier, customers had to call support teams, wait in queues, or search through long FAQ pages to get answers. Now, AI-powered chatbots and virtual assistants can handle many common banking questions instantly.

For example, customers can ask:

“What is my current balance?”

“Why was my card declined?”

“How do I reset my password?”

AI can answer these questions, guide customers through simple steps, and help resolve issues faster.

AI also helps support teams internally. It can summarize customer history, suggest next-best actions, classify complaints, and help agents respond more accurately. This makes support faster for customers and easier for employees.

The main benefit is not just reduced workload. It is a better customer experience. When people are dealing with money, they want quick and clear answers. AI helps banks deliver that at scale.

2. AI Is Detecting Fraud Faster

Fraud detection is one of the strongest use cases of AI banking solutions.

Traditional fraud detection systems often work through fixed rules. For example, they may flag a transaction if it is above a certain amount or happens in a different country. These rules are useful, but they are not always enough.

AI can go deeper. It can study customer behavior, transaction history, device usage, login patterns, and payment activity to detect unusual behavior in real time.

For example, AI may detect:

- A customer logging in from an unusual device

- A sudden high-value transaction

- Multiple failed login attempts

- A transaction pattern that looks similar to known fraud cases

- A possible account takeover attempt

- A suspicious money transfer

This helps banks identify fraud before it causes major damage.

AI can also support anti-money laundering checks by monitoring large volumes of transactions and identifying suspicious patterns that may be difficult for humans to detect manually.

As financial fraud becomes more advanced, real-time AI-based monitoring will become even more important.

3. AI Is Making Loan Approvals Faster

Loan approvals can be slow because banks need to review income, credit history, documents, repayment capacity, risk level, and financial behavior. In many cases, this process involves a lot of manual work.

AI can help speed up this process.

It can analyze financial data, review documents, detect missing information, assess borrower risk, and help lenders make faster decisions. For customers, this means shorter waiting times. For banks, it means better efficiency and reduced manual workload.

AI can help with:

- Personal loan approvals

- Credit card applications

- Mortgage pre-screening

- Business loan assessment

- Buy now, pay later risk checks

- Small business lending

However, this is also one of the most sensitive areas of AI use. Loan decisions can directly affect people’s lives and businesses. So, banks must ensure that AI models are fair, explainable, and regularly tested for bias.

AI can support lending decisions, but financial institutions should not treat it as a blind decision-maker. Human oversight is still important, especially for complex or high-impact credit decisions.

4. AI Is Personalizing Banking Experiences

Most banking apps still show the same experience to every customer. But customers have different income levels, spending habits, goals, financial responsibilities, and risk profiles.

AI can help banks personalize the experience for each customer.

For example, an app may suggest:

- A better savings plan based on spending behavior

- A credit card that fits the customer’s lifestyle

- A warning about unusually high monthly expenses

- A reminder before a possible low-balance situation

- A relevant loan offer based on financial activity

- A personalized investment recommendation

This type of AI-powered banking experience can make financial services feel more helpful and less generic.

For banks and fintech companies, personalization can improve engagement, customer satisfaction, and product adoption. For customers, it can make money management easier and more practical.

The future of financial personalization will not be about sending more promotional offers. It will be about giving the right guidance at the right time.

5. AI Is Automating Back-Office Operations

A lot of banking work happens behind the scenes. Employees review documents, process applications, verify information, prepare reports, update records, and manage internal workflows.

Many of these tasks are repetitive and time-consuming.

AI can automate or assist with tasks such as:

- Document processing

- Data entry

- Form verification

- Report summarization

- Transaction classification

- Internal ticket routing

- Customer record updates

- Compliance documentation

For example, when a customer submits documents for a loan, AI can extract important information from salary slips, tax records, bank statements, and identity documents. It can check whether the required information is present and flag issues for human review.

This reduces manual effort, improves speed, and helps employees focus on more complex work.

Back-office automation may not always be visible to customers, but it has a major impact on service quality. Faster internal processes often lead to faster customer outcomes.

6. AI Is Strengthening Risk Management

Banks deal with many types of risk. These include credit risk, fraud risk, market risk, liquidity risk, operational risk, and cybersecurity risk.

AI can help banks monitor these risks more effectively.

For example, AI can identify early warning signs that a borrower may struggle to repay a loan. It can detect unusual transaction patterns that may signal fraud. It can analyze market trends that may affect investment portfolios. It can also help monitor internal operations for errors or delays.

AI helps risk teams by:

- Analyzing large volumes of data

- Identifying patterns humans may miss

- Predicting potential problems

- Prioritizing high-risk cases

- Supporting faster decision-making

- Improving monitoring accuracy

In simple terms, AI helps banks see risks earlier. This gives them more time to respond before a small issue becomes a serious problem.

7. AI Is Supporting Compliance and Regulatory Work

Banking is one of the most regulated industries. Financial institutions must follow strict rules related to customer identity, anti-money laundering, data privacy, consumer protection, credit decisions, and reporting.

Compliance teams often need to review large volumes of data, documents, and transactions. AI can make this work more efficient.

AI can help with:

- Know Your Customer checks

- Anti-money laundering monitoring

- Suspicious activity detection

- Regulatory reporting

- Policy document review

- Audit preparation

- Customer due diligence

- Risk classification

AI can also help monitor regulatory changes and summarize important updates for compliance teams.

However, compliance automation must be handled carefully. Banks need clear records, audit trails, explainable decisions, and human review for sensitive cases. Regulators need to understand how decisions are made, especially when AI affects customers directly.

8. AI Is Improving Wealth Management and Financial Advisory

AI is also changing wealth management and investment services.

Financial advisors often manage large amounts of information, including client goals, portfolio performance, market updates, risk profiles, and investment documents. AI can help summarize this information and provide useful insights.

For example, an AI assistant can explain:

- Why a portfolio changed in value

- How spending habits affect savings goals

- How market changes may affect financial planning

Robo-advisory platforms also use AI and algorithms to help customers invest based on their goals and risk tolerance.

Still, financial advice is a sensitive area. AI should support advisors and customers, but it must follow regulatory rules and avoid giving unsuitable recommendations.

Also Read: AI in Medical Supply Chain Management: Benefits, Use Cases, Challenges, & Future TrendsThe Role of Generative AI in Banking

Role of Generative AI in Banking

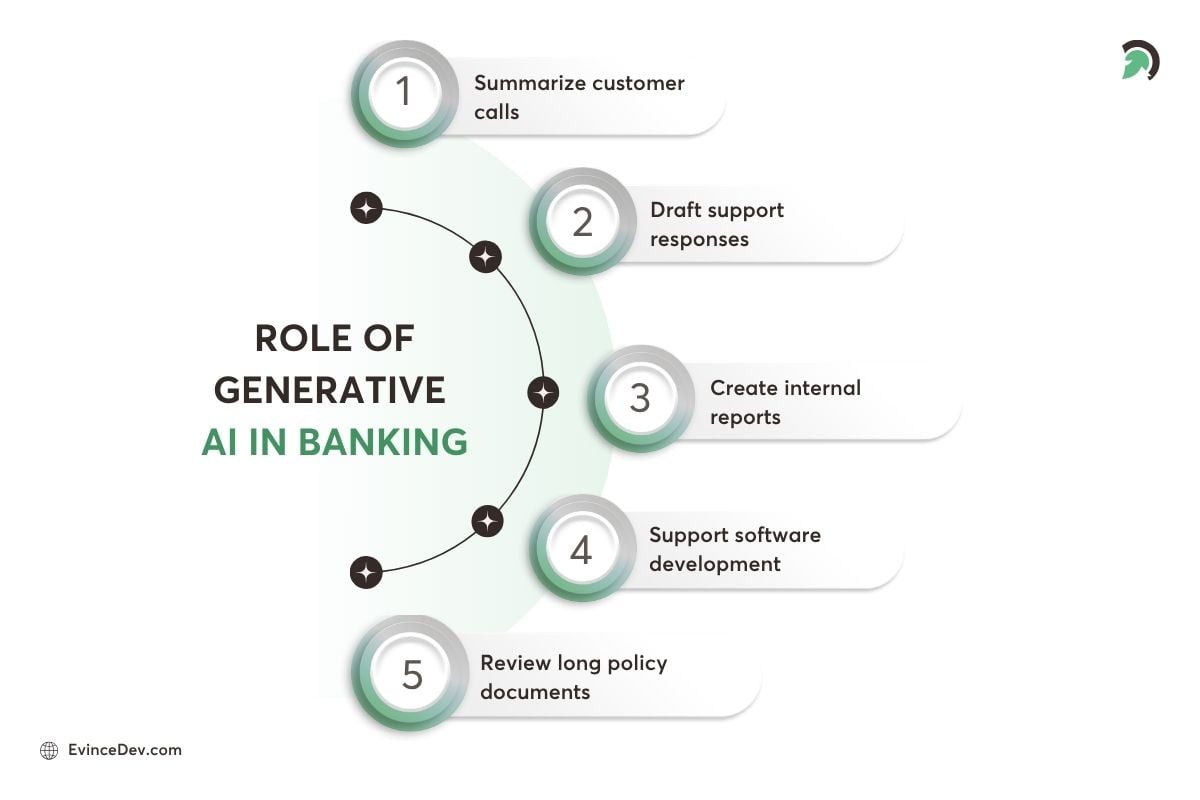

Generative AI is one of the most talked-about developments in finance. Unlike traditional AI systems that mainly classify, predict, or detect patterns, generative AI can create new text, summarize information, explain complex topics, and assist with decision-making workflows.

In banking, generative AI can be used to:

- Summarize customer calls

- Draft support responses

- Explain loan terms in simple language

- Create internal reports

- Prepare meeting notes for relationship managers

- Help employees search internal knowledge bases

- Support software development

- Generate compliance summaries

- Review long policy documents

For example, instead of asking an employee to read a long customer service history, generative AI can summarize the key issue, previous interactions, and possible next steps. This saves time and improves consistency.

But generative AI also comes with risks. It can sometimes produce incorrect or incomplete answers. In banking, even a small error can create confusion, compliance issues, or customer harm. That is why banks need approval workflows, human review, secure data access, and strong governance before using generative AI in high-impact areas.

Quick Stat:

NVIDIA’s 2025 State of AI in Financial Services report found that over half of surveyed financial services professionals were already using generative AI, up from 40% the previous year.

The Rise of AI Agents in Financial Services

AI agents are the next major step in financial technology.

A basic chatbot answers questions. An AI agent can go further and help complete a task.

For example, a banking AI agent may help a customer:

- File a transaction dispute

- Compare loan options

- Create a savings plan

- Cancel a lost card

- Prepare a budget

- Track monthly spending

- Set payment reminders

- Forecast business cash flow

For internal banking teams, AI agents can help route cases, gather documents, prepare reports, check policy requirements, and support operational workflows.

This can be powerful, but it also requires strong control. If AI can take action, banks need to define exactly what it is allowed to do. There should be permission limits, approval steps, activity logs, and human review for sensitive actions.

AI agents can make banking more efficient, but they must be designed with safety from the beginning.

Benefits of AI in Banking and Financial Sector

AI creates value for banks, fintech companies, and customers in different ways.

For banks, the major benefits include:

- Lower operational costs: AI reduces manual work and improves process efficiency.

- Faster decision-making: Teams can analyze data and respond to issues more quickly.

- Better fraud prevention: AI can detect suspicious behavior in real time.

- Improved compliance support: AI helps teams monitor transactions, review documents, and prepare reports.

- Higher employee productivity: Employees can spend less time on repetitive tasks and more time on strategic work.

For fintech companies, the benefits include:

- Faster innovation: AI helps fintech teams build smarter digital products.

- Scalable operations: AI can support growing customer volumes without increasing manual workload at the same pace.

- Better personalization: Fintech apps can deliver more relevant experiences based on user behavior.

- Stronger risk controls: AI can help manage fraud, lending risk, and customer verification.

- Improved customer engagement: AI-powered insights can make financial apps more useful and sticky.

For customers, the benefits include:

- Faster service: Customers can get answers and support more quickly.

- Safer transactions: AI can detect fraud and suspicious activity earlier.

- More personalized guidance: Customers can receive financial suggestions that match their behavior and goals.

- Easier access to finance: AI can help simplify applications, approvals, and onboarding.

- Better financial understanding: AI can explain complex financial information in simple language.

Also Read: How AI Helps B2B Businesses Improve Customer ExperienceQuick Stat:

PwC estimates that full front-to-back-office AI adoption could improve a bank’s efficiency ratio by up to 15 percentage points.

Challenges of AI in Banking

Even though AI has huge potential, financial institutions must handle it carefully. Banking is a high-trust industry. Customers expect their money, data, and financial decisions to be protected.

Here are the major challenges.

1. Data Privacy and Security

Banks handle sensitive personal and financial data. If AI systems use this data, it must be protected with strong security controls.

Financial institutions need to ensure that customer data is not exposed, misused, or shared without permission. They also need clear rules around which data AI systems can access.

2. Bias in AI Decisions

AI models learn from historical data. If that data includes bias, the AI system may repeat or even increase that bias.

This is especially risky in lending, credit scoring, insurance, and investment recommendations.

Banks must test AI models regularly to ensure decisions are fair and do not harm specific customer groups.

3. Lack of Explainability

In finance, it is not enough for AI to give an answer. Banks often need to explain how that answer was reached.

For example, if a loan is rejected, the customer and regulator may need a clear explanation. If AI flags a transaction as suspicious, the bank should understand why.

Explainability is important for trust, compliance, and accountability.

4. Legacy Banking Systems

Many banks still operate on old systems that were not designed for modern AI use. These legacy systems may have disconnected data, limited integration options, and slow update cycles.

Before banks can scale AI properly, they may need better APIs, cloud infrastructure, data pipelines, and secure integrations.

This is where working with the right technology partner becomes important, especially for institutions that need custom fintech software development services or want to modernize existing platforms.

5. Regulatory Compliance

AI must operate within banking regulations. Financial institutions need to ensure that AI systems follow laws around privacy, consumer protection, credit decisions, fraud monitoring, and financial advice.

This requires proper documentation, audit trails, governance policies, and regular reviews.

6. Cybersecurity Risks

As banks use more AI, attackers may also look for new ways to exploit AI systems.

Risks can include fake identities, deepfake fraud, prompt manipulation, data leaks, and attacks on AI models. Banks need cybersecurity strategies that specifically account for AI-related threats.

7. Talent and Skill Gaps

AI adoption requires skilled teams. Banks need data scientists, AI engineers, compliance experts, cybersecurity professionals, product leaders, and domain specialists who understand both finance and technology.

Without the right skills, AI projects may remain stuck in pilot stages and fail to deliver real business value.

8. Customer Trust

Trust is the foundation of banking. Customers may hesitate to rely on AI if they do not understand how it works or worry that it may make unfair decisions.

Banks need to be transparent about how AI is used, where humans are involved, and how customer data is protected.

How Banks and Fintech Companies Can Prepare for AI Adoption

AI adoption should not start with technology alone. It should start with business goals, customer needs, data readiness, and risk controls.

Here is a practical roadmap.

1. Start with the Right Use Cases

Banks should begin with use cases that offer clear value and manageable risk.

Good starting points may include customer service support, document processing, internal knowledge search, fraud alerts, and operational automation.

High-risk areas like credit decisions, investment advice, and fraud blocking need stronger oversight and careful testing.

2. Clean and Organize Financial Data

AI depends on data quality. If the data is inaccurate, incomplete, outdated, or disconnected, AI results will not be reliable.

Financial institutions should invest in data cleaning, governance, secure storage, and system integration before scaling AI.

3. Modernize Legacy Systems

AI works best when systems are connected. Banks may need to modernize outdated platforms, build APIs, improve data pipelines, and move selected workloads to secure cloud environments.

This does not mean every legacy system must be replaced immediately. But banks need a clear modernization plan that supports future AI use.

4. Build Strong AI Governance

For banks and fintech companies, AI governance is not just a technical requirement. It is a way to make sure AI is used safely, responsibly, and in line with regulatory expectations.

Strong governance means having clear rules for how AI systems are designed, tested, deployed, monitored, and improved over time. Before using AI in areas like lending, fraud detection, customer support, or compliance, financial institutions need to define how customer data will be protected, how bias will be tested, how decisions will be explained, and where human review will be required.

It also includes classifying AI use cases based on risk, monitoring model performance regularly, maintaining audit trails, documenting compliance requirements, and setting approval workflows for sensitive actions.

5. Keep Humans in the Loop

AI can support decisions, but not every decision should be fully automated.

Sensitive areas like loan rejection, fraud investigation, complaints, account freezes, and investment advice should include human review or clear escalation paths.

The goal should be human plus AI, not human versus AI.

Expert View:

The strongest banking AI systems will not remove humans completely. They will combine AI speed with human judgment, especially in high-impact areas like loan rejection, account freezes, fraud disputes, and investment guidance.

6. Choose the Right Technology Partner

AI adoption in banking requires more than technical development. It requires financial domain understanding, secure architecture, compliance awareness, scalable engineering, and long-term support.

A reliable custom software development company can help banks and fintech companies assess AI readiness, choose the right use cases, modernize systems, and build secure digital products.

For more advanced needs, businesses may also require custom AI development services to build AI models, automation tools, intelligent assistants, fraud detection systems, or AI-powered financial platforms.

Expert View:

AI adoption should not begin with tools. It should begin with readiness. Banks need clean data, secure integrations, modern infrastructure, and clear ownership before scaling AI across customer-facing or decision-heavy workflows.

Bottom Line

AI is changing banking and fintech in a major way. It is helping financial institutions improve customer service, detect fraud faster, personalize experiences, automate operations, manage risk, and support better decision-making.

But AI should not be used blindly. Banking is too important, too regulated, and too personal for uncontrolled automation.

The real opportunity is to use AI carefully and strategically. Banks and fintech companies should start with the right use cases, prepare their data, modernize their systems, build strong governance, and keep humans involved in critical decisions.

AI will not replace banking. It will reshape how banking works.

At EvinceDev, we help financial businesses build secure, scalable, and AI-ready digital solutions that support innovation without losing focus on trust, compliance, and long-term reliability.

The financial institutions that succeed will be the ones that use AI to become faster, safer, more transparent, and more customer-focused.