Key Takeaways:

- Security First: Encryption, biometric login, and continuous monitoring protect users and prevent fraud.

- Regulatory Ready: KYC and AML compliance are mandatory to operate legally across financial markets.

- User Experience: Simple onboarding and fast transactions drive adoption and long term retention.

- Monetization Model: Revenue comes from transaction fees, merchant partnerships, and value added services.

- Market Fit: Success depends on solving real payment problems for target users and regions.

A few years ago, the process of making a payment for essential items involved paying in cash, standing in queues, and sometimes even calculating change. Even digital payments were time-consuming, with a number of steps, passwords, and redirects involved. Today, a single tap on your mobile device allows you to pay bills, transfer money, or split expenses. What has changed is not technology, but how money ought to move.

Digital wallets emerged quietly as a solution to this growing need for speed and simplicity. At first, they were just a convenient alternative to cards and cash. Over time, they evolved into full-scale financial platforms, bringing payments, rewards, identity verification, and financial services into a single app. For users, this meant fewer friction points. For businesses, it opened the door to faster transactions, deeper customer engagement, and new revenue opportunities.

Behind this seamless experience, however, lies a complex ecosystem of technology, security, and compliance. Digital wallet platforms are a core part of modern FinTech software development, where payments, compliance, and intelligent risk systems converge.

Building a digital wallet is not simply about enabling payments. It deals with trust-oriented user experience design, bank integration, and the protection of critical user data.

In this guide, we will walk through the essentials of building a digital wallet mobile application that users trust, regulators approve, and businesses can scale.

Market Insight:

According to Juniper Research, digital wallet users are expected to grow from 4.4 billion in 2025 to over 6 billion by 2030, a 35% increase in five years, making wallet products a strong long-term investment for businesses.

What Is a Digital Wallet?

A digital wallet, also known as an eWallet, is a software-based application that allows users to store money digitally and make electronic transactions without using physical cash or cards. Digital wallets securely store payment credentials, such as debit and credit cards, bank account details, and, in some cases, digital currencies, enabling users to pay for goods and services using their smartphones or web applications.

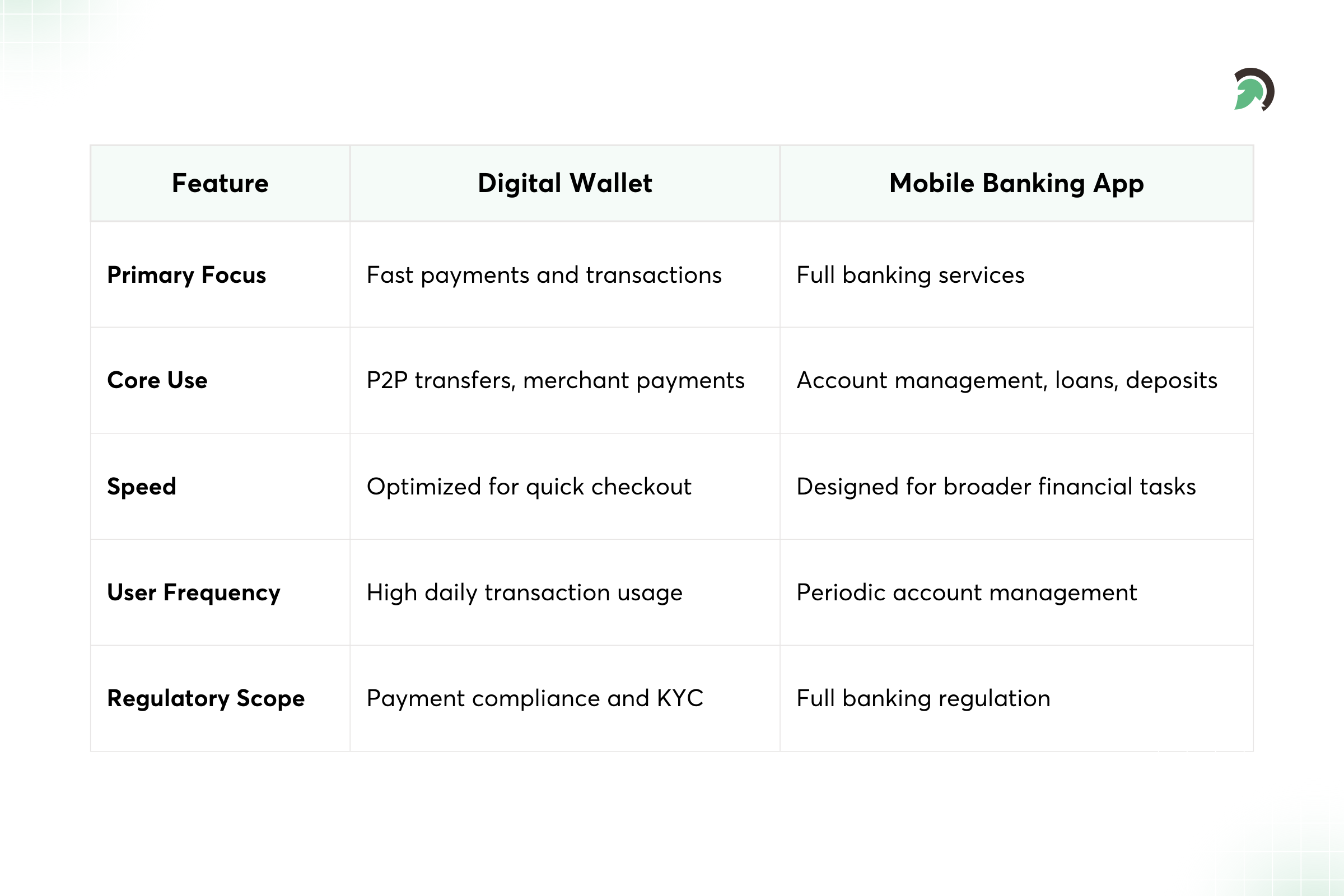

Unlike traditional banking apps that focus primarily on account management, digital wallets are built around fast, convenient, and frequent transactions. They act as an intermediary between users, merchants, and financial institutions, simplifying payments for everyday use cases such as online shopping, in-store purchases, bill payments, peer-to-peer transfers, subscriptions, and more.

Digital wallets have become increasingly fundamental to financial services. With the increased use of smartphones, improved connectivity, and greater trust in digital money, digital wallets have changed how people relate to money. Digital wallets are used not only for making payments but also for rewards, financial services, or even digital identities.

Quick Stat:

According to McKinsey’s 2024 consumer digital payments survey, 92% of US consumers made some form of digital payment in the past year, reinforcing why digital wallets have become a core payment method rather than an optional feature.

What Are the Different Types of Mobile Wallet Apps?

Digital wallet apps can be categorized based on how funds are stored, used, and withdrawn. Understanding these types is important when planning a digital mobile wallet application, as each type has different regulatory, technical, and business requirements.

-

Closed Wallets

There is one company that provides closed wallets usable only within its ecosystem. If the wallet is closed, it is not possible to withdraw the funds to an actual bank account or use them in any other way. Online transaction systems offering wallet amounts as cashback, store credit, or other forms of credit after purchases made through their systems are examples of closed wallets.

-

Semi-Closed Wallets

Semi-closed wallets enable customers to make payments at a shortlist of merchants and/or service providers. However, customers will not be allowed to withdraw the cash to their own bank account. These wallets are generally adopted for retail payments, food orders, taxi orders, and online services. They strike a balance between usability and complexity.

-

Open Wallets

Open wallets offer the most flexibility. Users can add money, make payments, and withdraw funds to their bank accounts. These wallets usually require partnerships with banks or financial institutions and are subject to strict regulatory compliance. Open wallets are ideal for large-scale payment platforms and FinTech products offering broad financial services.

-

Cryptocurrency Wallets

Crypto wallets store digital assets such as Bitcoin or Ethereum. They can be custodial or non-custodial and often focus on blockchain security, private key management, and decentralized transactions.

-

White Label Wallets

White-label eWallet app development solutions are pre-built platforms customized for businesses. They reduce time-to-market while still allowing branding and feature customization.

Advantages of Digital Wallet App Development

Investing in digital wallet app development offers benefits for both businesses and end users.

-

Convenience and Speed

Wallet apps enable instant transactions, eliminating the need for physical cash or cards. Payments can be completed in seconds using mobile devices.

-

Improve Customer Experience

Seamless onboarding, fast payments, and real-time notifications improve user satisfaction and engagement.

-

Business Growth and Retention

Wallets encourage repeat usage through cashback, rewards, and loyalty programs. They also help businesses capture valuable transaction data.

-

Reduced Operational Costs

Digital payments reduce cash handling, reconciliation efforts, and manual errors.

-

Financial Inclusion

Wallet apps provide access to digital payments for underbanked populations who may not have access to traditional banking services.

-

Scalability

Once built, digital wallets can scale rapidly across regions, users, and merchants with relatively low incremental costs.

Market Insight:

The Federal Reserve Payments Study estimates mobile wallet payments climbed from 2.9 billion transactions in 2018 to 14.4 billion in 2022, reinforcing why businesses are investing heavily in wallet-ready checkout and payment experiences.

Features of Mobile Wallet Apps

A successful digital wallet app combines essential payment functionality with a secure and user-friendly experience.

- User Registration and Authentication: Secure onboarding using mobile numbers, email, OTP verification, PINs, or biometric authentication.

- Wallet Balance Management: Users can view available balance, transaction history, and pending payments in real-time.

- Add Money and Withdraw Funds: Integration with banks, cards, and payment gateways to support top-ups and withdrawals.

- Peer to Peer Transfers: Instant money transfers between users using phone numbers, usernames, or QR codes.

- Merchant Payments: Support for in-app payments, QR code scanning, NFC, and online checkout integrations.

- Transaction History and Receipts: Detailed records of all transactions with timestamps, statuses, and downloadable receipts.

- Notifications and Alerts: Push notifications, SMS, or email alerts for payments, refunds, and suspicious activity.

- Offers, Rewards, and Cashback: Built in promotional features to boost engagement and retention.

- Customer Support: In app chat, ticketing systems, and dispute resolution tools.

Key User Flows in a Wallet App

Clear and frictionless user flows are critical to wallet adoption and trust.

- Onboarding and Registration Flow: Users sign up, verify their identity, set security credentials, and agree to terms.

- KYC Verification Flow: Identity verification using documents, selfies, or digital verification APIs to meet regulatory requirements.

- Add Money Flow: Users choose a funding source, enter an amount, and complete the payment securely.

- Send Money Flow: Users select a recipient, enter the amount, review details, and confirm the transfer.

- Scan and Pay Flow: Users scan a merchant QR code, enter the amount, and complete payment instantly.

- Refund and Reversal Flow: Clear processes for failed payments, refunds, and chargebacks to maintain user trust.

How to Create a Digital Wallet App?

eWallet app development requires a structured approach due to real-money transactions, sensitive user data, and regulatory compliance requirements.

Here is a simple step-by-step guide to the mobile wallet app development process.

-

Step 1: Define the Business Model

Determine who the application is for and what issue it tries to resolve. Lock down the wallet form (closed, semi-closed, or open), functional scenarios (P2P, merchant transactions, or billing), geographic regions, and implementation strategies that generate revenue from fees, commissions, or sponsorship.

-

Step 2: Understand Regulatory Requirements

Check the compliance requirements for your region, including KYC, AML, licensing, transaction limits, and data protection rules. Plan when and how user verification should happen to avoid product changes later.

-

Step 3: Design User Experience

Create a clean, fast user journey for sign-up, KYC, adding money, sending money, and paying merchants. Keep payment steps minimal, provide clear confirmations, and ensure users can easily track transaction status.

-

Step 4: Develop Core Functionality

Build the core modules: user accounts, wallet balance, transaction processing, transaction history, notifications, and an admin panel. A strong ledger and reporting setup help keep wallet records accurate.

-

Step 5: Integrate Payment Providers

Integrate payment gateways, banking APIs, card networks, or local payment rails based on your market. Set up webhooks for payment updates and add safeguards to prevent failed or duplicate transactions.

-

Step 6: Test Thoroughly

Test all key flows, including success and failure cases, refunds, and reversals. Include security testing and performance testing to ensure the app stays stable under high usage.

-

Step 7: Launch and Monitor

Launch with monitoring in place for transaction success rates, errors, and suspicious activity. Gather user feedback, fix issues quickly, and improve features through regular updates.

Challenges in Developing a Mobile Wallet App

- Security Risks: Wallet apps are prime targets for fraud, hacking, and data breaches.

- Regulatory Complexity: Compliance requirements vary across regions and can change frequently.

- Payment Failures and Downtime: Dependence on third-party services requires strong error handling and retries.

- User Trust: Any failure or security incident can significantly impact adoption.

Security and Compliance Checklist for Wallet Apps

A strong security and compliance framework is non-negotiable for wallet apps. Here is a practical checklist to cover the essentials:

- Encryption in transit and at rest: Use TLS for network traffic and encrypt sensitive data in storage and backups.

- Secure authentication and authorization: OTP or 2FA, strong PIN rules, biometric login options, and role-based access for admin users.

- Security audits and penetration testing: Regular vulnerability scans, pen tests, and timely patching.

- KYC and AML processes: Identity verification, KYC status tracking, and transaction limits based on verification level.

- Transaction monitoring and fraud detection: Alerts for suspicious behavior, velocity limits, and risk-based checks.

- Data protection compliance: Follow local privacy laws, consent requirements, and retention policies.

- Audit logs and reporting: Detailed logs for user actions and transactions for compliance and dispute handling.

- Disaster recovery and incident response: Backups, failover planning, monitoring, and a defined incident response process.

How to Choose the Right Digital Wallet Development Partner

Selecting the right development partner plays a major role in how secure, scalable, and successful your wallet app will be. Here are the key factors to evaluate:

- Proven FinTech experience: Choose a team with hands-on experience building wallet apps, payment platforms, or similar FinTech products, not just general app development.

- Strong security practices: The partner should follow secure development standards, implement encryption and fraud controls, and support regular audits and penetration testing.

- Regulatory awareness: They should understand KYC, AML, data privacy, and other compliance requirements for your target market, and build workflows that align with them.

- Scalable architecture approach: Look for a team that designs reliable systems for high transaction volumes, with clean APIs, strong logging, and performance-focused infrastructure.

- Post-launch support: A good partner stays involved after release with monitoring, bug fixes, security patches, performance improvements, and feature upgrades.

Conclusion

Digital wallet apps have become a foundational part of modern digital economies. From enabling fast payments to supporting financial inclusion and driving business growth, wallets offer immense value when built correctly. However, developing a digital wallet application involves far more than building an app. It requires a clear strategy, strong security measures, and strict regulatory compliance. A solid understanding of wallet types, features, and technical considerations is essential.

With the right strategy and development partner, a digital wallet app can become a powerful engine for innovation, customer engagement, and long-term success. If you are looking to build or scale a wallet solution, EvinceDev supports businesses with end-to-end digital wallet app development, including product strategy, UI UX, secure architecture, payment gateway and banking integrations, KYC workflows, and ongoing maintenance and support, helping teams launch reliable payment experiences with confidence.