Key Takeaways:

- KYC Onboarding Essentials: Know customer identity with document checks, biometrics, and risk-based profiling for safer access.

- AML Monitoring That Works: Use transaction monitoring plus case management to catch suspicious patterns and support SAR handling.

- PSD2 Security for APIs: Design strong authentication and consent-driven open banking API access to meet payment expectations.

- DORA Resilience Engineering: Build ICT risk controls, incident readiness, and vendor management so outages don’t become liabilities.

- Automation Beats Manual: Automate KYC/AML workflows and evidence capture to reduce errors and speed up regulatory reporting.

- Compliance by Design: Treat compliance as product infrastructure—data models, logging, and release controls from day one.

- Audit Evidence Must Exist: Capture decisions and monitoring outcomes so you can explain controls clearly during reviews.

- Privacy-First Controls: Minimize PII, encrypt sensitive data, and manage retention to align security with regulatory expectations.

FinTech compliance is the foundation that helps digital financial products stay secure, legal, and scalable. Whether you are building onboarding flows, enabling payments, or connecting third-party financial services, your product operates inside a regulatory environment that demands strong controls every day.

That is why compliance is not just documentation or policy work. It is an operational discipline built into how a product verifies users, detects risk, protects data, and responds to failures in real-world conditions. In practice, fintech compliance shapes everything from customer onboarding to transaction monitoring, authentication, reporting, and ongoing risk management.

In this guide, we break down the key frameworks that fintech companies must understand, including KYC, AML, PSD2, and DORA. We also explain how compliance teams, tools, and processes fit into the FinTech software development lifecycle, from early product design to steady-state operations.

As regulatory expectations continue to evolve across regions, businesses are expected to show more than policies. They must prove that effective controls are active in production. When done well, fintech compliance supports safer onboarding, stronger trust, lower risk exposure, and smoother growth across products and markets.

What is Fintech Compliance?

Fintech compliance refers to the processes, technologies, and controls used by financial platforms to meet regulatory requirements. These include identity verification, transaction monitoring, data protection, and risk management.

Regulation defines what must be followed, compliance ensures it is implemented, governance determines how decisions are made, and accountability is managed over time.

Compliance is a critical component of building secure fintech platforms during fintech software development.

Key Differences Between KYC, AML, PSD2 & DORA

These frameworks often get lumped together in technology, but they solve distinct focus areas:

- KYC: Where identity must start and when assurance should be rechecked.

- AML: When and how to monitor transactions, then escalate to authorities.

- PSD2: Design rules governing account access and identity-linked payment processing are stricter.

- DORA: The principles behind managing ICT risk and third parties.

Elevator pitch:

- Primary goal – KYC: “Trust who you’re doing business with.” | AML: “Don’t let them move money here.” | PSD2: “Give access, safely.” | DORA: “You can rely on this.”

- Location – KYC/AML: customer journey and financial crime unit | PSD2: engineering, payment processing, and open APIs | DORA: vendors, ICT, and operational resilience.

- Audit focus – Evidence of verification (KYC), monitoring + case handling (AML), payment consent APIs (PSD2), and meeting vendor requirements (DORA).

What Is KYC in FinTech?

KYC (Know Your Customer) ensures that businesses verify users’ identities before granting financial access. It helps prevent fraud, identity theft, and unauthorized transactions.

The process typically includes document verification, biometric checks, and risk profiling. Many fintech platforms also implement ongoing monitoring to detect changes in user behavior.

To scale onboarding efficiently, businesses often use KYC AML automation software that reduces manual effort and improves accuracy.

What Is AML in FinTech?

AML (Anti-Money Laundering) focuses on detecting and preventing illegal financial activities such as money laundering and fraud.

It involves continuous transaction monitoring, risk scoring, and alert generation. Suspicious activities are flagged and investigated based on predefined rules and behavioral patterns.

These systems are typically part of broader fintech risk management software designed to reduce exposure to financial crime and ensure regulatory compliance.

PSD2 & API Security

PSD2 regulates secure access to financial data and enables open banking through APIs. It ensures that third-party providers can access financial information safely with user consent.

Strong customer authentication and encrypted API communication are key requirements. Businesses must maintain audit-ready API documentation and secure data flows.

These requirements play a critical role in modern payment system development, especially in API-driven financial ecosystems.

Fintech Compliance Technology & Tools

Modern fintech compliance software solutions combine identity, risk analytics, and governance controls into a stack. Look for systems that are audit-friendly and make it easy to explain why a decision was made.

Identity verification tools (OCR, biometrics)

- OCR: fast, solid read rates on various IDs.

- Biometric/liveness: ability to detect spoofing; enough choices of signals for you to train on.

- Fraud signals: enough signals for you to control how fast you want to be vs false positives.

Transaction monitoring systems

It’s becoming common and needed to train systems on customer risk, so not all alerts are treated equally. It’s worth adding to your RfI/RfP list how well each vendor:

- supports research and rules simultaneously

- lets you see audit trails of why an alert fired

AI-based fraud detection

You can’t measure what you can’t explain. Your AI system must start with your rules. Not your model’s rules, your rules. It must show when it exceeds and trips that wire. Lastly, it must build a feedback loop that retrains when it gets something wrong.

API security and encryption

Shows like PSD2 mentioned open banking APIs as well as payment access. If API documentation exists, you can be sure auditors will ask to see it. Make sure you can prove your entire flow and are not just relying on black-box documentation.

RegTech solutions

Software popping up in this space typically focuses on reporting. They’re gaining popularity because nobody enjoys having a bunch of new employees just for producing documents.

Compliance Challenges in Fintech

Fintech companies face multiple compliance challenges while building secure, scalable, and regulation-ready financial products. These challenges affect product development, customer onboarding, operations, and long-term growth.

-

High Implementation Costs

Building compliant fintech systems requires investment in identity verification, AML monitoring, fraud detection, encryption, reporting tools, and audit processes. These costs continue after launch through maintenance, compliance updates, and ongoing operational support.

-

Cross-Border Compliance Complexity

Each country or region has different rules for customer verification, transaction monitoring, reporting, and data handling. This makes it more difficult for fintech companies to expand globally while maintaining consistent compliance standards.

-

Balancing UX with Strict Verification

FinTech products must prevent fraud without creating too much friction for genuine users. Businesses need to balance strong verification processes with smooth onboarding and transaction experiences to improve both compliance and customer conversion.

-

Evolving Regulations

Financial regulations change frequently as technology, risks, and market expectations evolve. Fintech companies must regularly update policies, workflows, and systems to stay aligned with new legal, security, and operational requirements.

-

Data Privacy Concerns

Compliance systems handle sensitive customer and financial data. Businesses must use secure storage, controlled access, data minimization, and privacy-focused processes to meet regulations and protect user trust.

Best Practices for Fintech Compliance

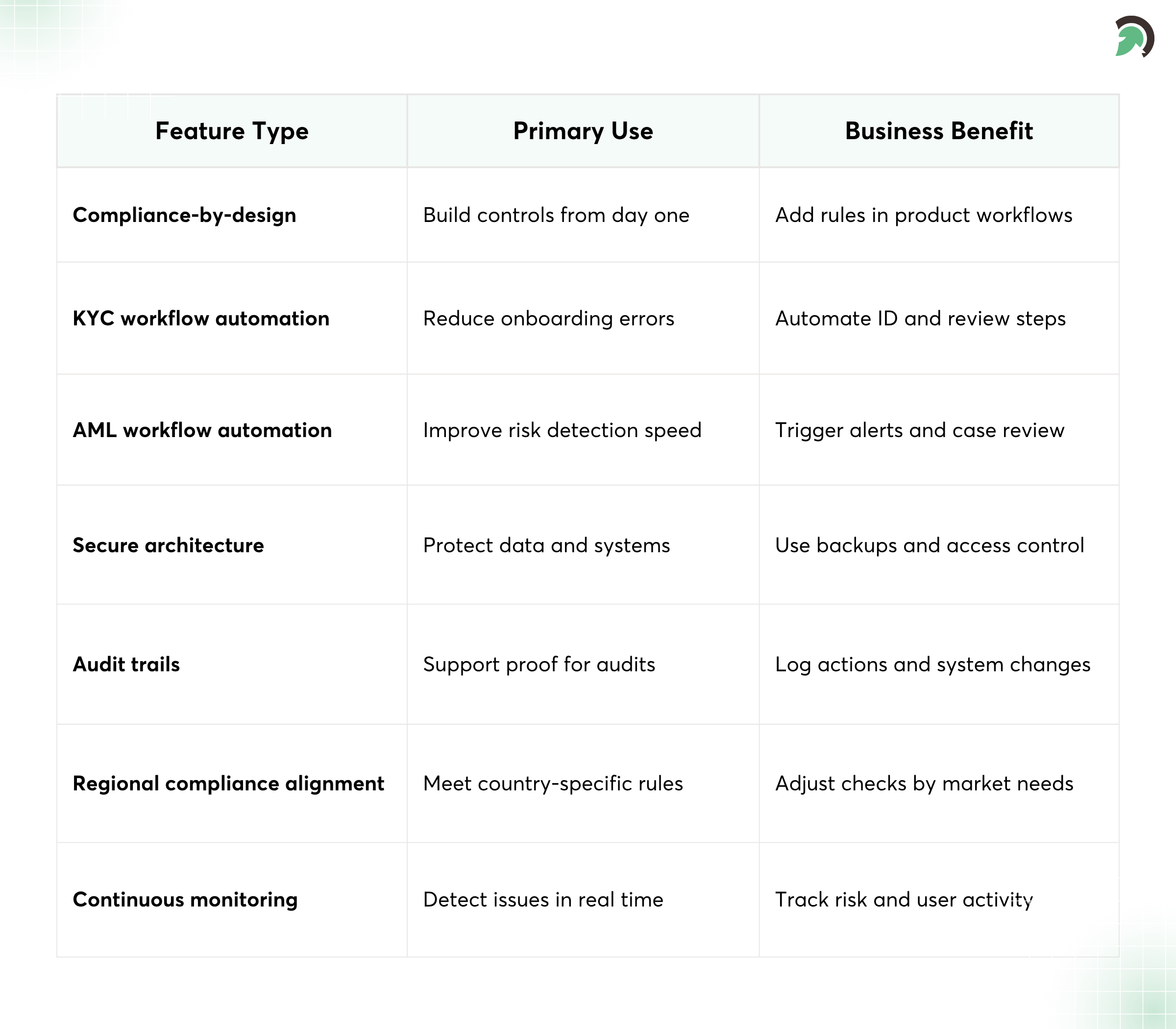

1. Implement a compliance-by-design approach

It must engineer a mechanism to ensure the business meets requirements at the end of every sprint. This means controls are built with the product in:

- the right requirements

- the right data

- the right logs

- the right reports

2. Automate KYC and AML workflows

The more manual, the more human error. Both of these areas require significant human assistance after the software makes a decision. Each has some triggers, like high-risk customers triggering AML monitoring. Automate that decision and the report.

3. Use a secure and scalable architecture

- automatic backups

- per-key, per-contact access controls

- exportable and verifiable identity, entity, and product requirements

- notifications of anything anyone might need to know

4. Conduct regular audits and updates

Prove this by the paper trail you leave on incidents, including identity fraud or any new AML regulations. In fintech, something you implement will almost always be your best snitches for when you need proof you were on your best behavior.

5. Stay aligned with regional regulations

The real work of compliance is recognizing that these roll out in perpetuity rather than on a per-project basis. Have a product manager own this and write the product roadmap so the engineering doesn’t forget what’s coming three sprints away.

Businesses looking to streamline compliance workflows can explore tailored fintech solutions designed for security and scalability.

Role of RegTech in Modern Compliance

RegTech refers to technology solutions designed to simplify compliance processes through automation and real-time monitoring.

These tools help businesses:

-

Automate Reporting

Automated reporting tools streamline the collection, processing, and submission of compliance data. They reduce manual effort, minimize human errors, and ensure timely regulatory filings. These systems generate standardized reports, maintain consistency, and help businesses stay audit-ready while adapting quickly to changing compliance requirements across different regions and financial regulations.

-

Monitor Transactions

Transaction monitoring systems analyze financial activities in real time to detect suspicious behavior and potential fraud. They use predefined rules, risk scoring, and behavioral analytics to flag anomalies. This enables faster investigation, reduces financial crime risks, and ensures compliance with AML regulations while maintaining a secure and transparent transaction environment.

-

Maintain Audit Trails

Audit trail systems record every compliance-related action, including user activity, system changes, and transaction history. These logs provide clear evidence during audits, improve accountability, and support regulatory investigations. Well-maintained audit trails help organizations demonstrate transparency, trace decisions, and ensure compliance with evolving financial and data governance standards.

-

Reduce Manual Workload

RegTech solutions automate repetitive compliance tasks such as data verification, risk assessment, and reporting. This reduces dependency on manual processes, improves operational efficiency, and allows teams to focus on strategic decision-making. Automation also enhances accuracy, speeds up workflows, and ensures consistent compliance execution across financial systems.

RegTech solutions are often integrated into broader fintech product development strategies to improve efficiency and regulatory alignment.

Cost Factors in Fintech Compliance Implementation

Cost for fintech companies breaks down to:

-

Technology Infrastructure

Costs include encryption systems, identity verification tools, transaction monitoring platforms, secure cloud infrastructure, and data protection mechanisms needed to support compliance, fraud prevention, and audit readiness.

-

Third-Party Integrations

Fintech companies often rely on third-party providers for KYC, AML screening, payment processing, fraud detection, and reporting tools, which adds recurring integration, licensing, and maintenance costs.

-

Regulatory Requirements by Region

Compliance costs vary by region because each market has different regulatory standards, reporting obligations, identity verification rules, and operational requirements that influence product design and compliance processes.

-

Ongoing Monitoring and Audits

Compliance is an ongoing investment that includes continuous transaction monitoring, policy updates, internal reviews, external audits, staff training, and documentation needed to maintain regulatory alignment.

Future Trends in Fintech Compliance

-

AI-Powered Compliance Automation

AI-powered compliance automation helps fintech companies detect risks faster, automate repetitive checks, improve reporting accuracy, and strengthen decision-making across KYC, AML, fraud detection, and regulatory workflows.

-

Real-Time Monitoring

Real-time monitoring enables businesses to identify suspicious transactions, policy violations, and risk events immediately, helping compliance teams respond faster and maintain stronger operational control.

-

Global Regulatory Standardization

Global regulatory standardization may gradually reduce compliance complexity by aligning financial rules across regions, making it easier for fintech companies to scale products across international markets.

-

Privacy-First Financial Systems

Privacy-first financial systems focus on data minimization, secure access controls, and transparent data handling practices to meet regulatory expectations while protecting customer trust.

Why Compliance Expertise Matters

Compliance plays a crucial role in building trust and ensuring long-term business sustainability. Poor compliance can lead to penalties, operational disruptions, and loss of credibility.

On the other hand, strong compliance enables secure growth, smooth operations, and customer confidence. Businesses that prioritize compliance early can scale faster and enter new markets with fewer risks.

- Penalties and legal risks don’t build your business.

- Customer trust does.

- When they let you keep transacting, you know you’ve struck the balance between verifying and converting.

- Room to grow means not having to slow down, even though you ignored bone spurs in the early days.

- Secure innovation is the new sexy in breach wear.

What can software developers do to avoid the rush of new fintech companies that subsequently slam on the brakes on customer acquisition, while they appear to use the same engineering team to meet compliance requirements?

Conclusion

FinTech compliance is no longer just a regulatory requirement. It is a foundation for building secure, scalable, and trustworthy financial products. A well-defined compliance blueprint that integrates KYC, AML, and DORA helps businesses reduce risk, strengthen fraud prevention, and maintain operational resilience in an evolving regulatory landscape.

As FinTech ecosystems continue to grow, organizations that prioritize compliance early will be better positioned to scale confidently, enter new markets, and earn long-term customer trust. Aligning technology, processes, and compliance frameworks is key to achieving this balance.

If you are planning to build or enhance a compliant FinTech solution, working with experienced partners can make a significant difference. EvinceDev helps businesses design and implement secure, future-ready fintech platforms aligned with global compliance standards. Explore how EvinceDev can support your compliance journey and help you build with confidence in a rapidly changing financial environment.