Key Takeaways:

- Architecture Matters: A strong architectural foundation supports security, scalability, compliance, and reliable financial operations.

- Built-In Security: Fintech systems need architecture that supports data protection, regulatory requirements, and risk control from the start.

- Scalable Systems: Modern fintech platforms need flexible architectures that can handle growing users, transactions, and integrations.

- Different Needs: Payment apps, lending platforms, neobanks, and trading systems each require different architectural priorities.

- Right Tech Stack: The right mix of APIs, cloud infrastructure, databases, and services helps fintech products grow efficiently and stay resilient.

FinTech products operate in one of the most sensitive and complex digital environments. Unlike traditional applications, they deal with real money, regulatory scrutiny, and high user expectations for speed and reliability. This makes architecture not just a technical concern, but a critical business foundation.

A well-designed system ensures that transactions are processed securely, data flows seamlessly, and systems scale efficiently as demand grows. Poor architecture, on the other hand, can lead to security vulnerabilities, downtime, compliance failures, and loss of customer trust.

At the core of every successful financial product lies a robust FinTech software architecture that defines how different components interact, how data is managed, and how systems evolve over time.

This blog explores how FinTech systems are structured and built, covering key components, architecture patterns, and the step-by-step process behind modern financial platforms.

Quick Stat:

According to Boston Consulting Group (BCG) and QED Investors, FinTech revenues are projected to grow from $245 billion to $1.5 trillion by 2030, highlighting the scale and speed at which modern financial platforms are evolving.

What Is FinTech Software Architecture?

FinTech architecture refers to the structural design of a financial system, including its components, data flow, integrations, and infrastructure. It serves as a blueprint for how the system is developed, deployed, and scaled.

Unlike general applications, FinTech systems must account for:

- Real-time transaction processing

- High security standards

- Complex integrations with banking systems

- Regulatory compliance

While development focuses on writing code and building features, architecture determines how those features work together as a cohesive system. This is where FinTech software development architecture becomes critical, as it ensures that business requirements align with technical capabilities.

Beyond technical design, architecture also supports business goals such as faster product launches, better user experiences, and long-term scalability. In many ways, it becomes a strategic asset rather than just a technical framework.

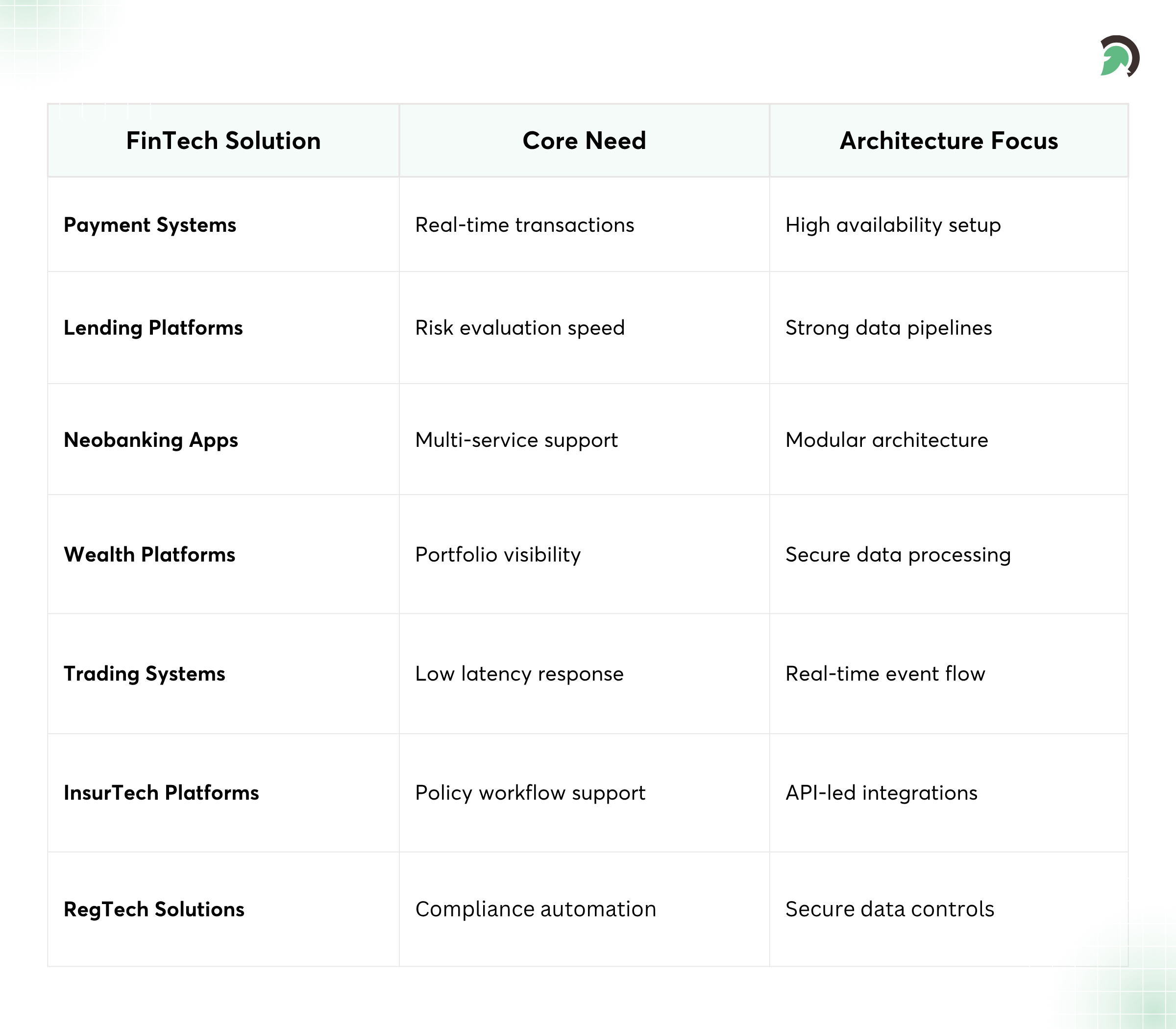

Types of FinTech Systems & Their Architecture Needs

Different types of FinTech products require different architectural approaches based on their functionality, scale, and performance expectations.

Payment systems are designed for real-time processing and must support high availability. Even minor delays or downtime can directly impact transactions and user trust, making performance and reliability critical.

Lending platforms rely heavily on data processing and risk evaluation. These systems often include advanced scoring engines and require strong data pipelines to handle large volumes of financial and behavioral data efficiently.

Neobanks operate as full-stack financial platforms, combining multiple services such as payments, savings, and lending. Their architecture must support modularity, scalability, and seamless integration across services.

Wealth management and trading applications prioritize low latency and real-time data delivery. These systems must process market data instantly while ensuring accuracy and responsiveness.

Understanding these differences helps in designing more effective FinTech software solutions tailored to specific business needs.

Key Requirements That Shape FinTech Architecture

-

Security-First Design

Security is the most important requirement in FinTech systems. Sensitive user data, financial transactions, and identity information must be protected at all times. This involves encryption, secure authentication methods, fraud detection systems, and continuous monitoring.

-

Regulatory Compliance

FinTech platforms must comply with regulations such as PCI DSS, KYC, AML, and GDPR. These requirements influence how data is stored, processed, and accessed. For example, systems often integrate KYC AML automation software to streamline identity verification while maintaining compliance.

-

Scalability and Performance

FinTech applications must handle spikes in transactions, especially during peak usage times. A scalable FinTech architecture ensures that systems can expand horizontally without compromising performance.

-

Reliability and Availability

Downtime in FinTech systems can lead to financial losses and reputational damage. High availability, failover mechanisms, and redundancy are essential to ensure uninterrupted service.

-

Trade-offs in System Design

One of the key insights in FinTech architecture is that no system can optimize security, scalability, and performance equally at all times. Trade-offs must be made based on business priorities, system requirements, and growth expectations.

Core Layers of FinTech Architecture

-

Presentation Layer

The presentation layer consists of interfaces such as mobile applications, web applications, and admin panels. The main objective of this layer is to ensure a smooth end-user experience, especially for crucial financial activities such as payments and transfers.

-

Application Layer

The backend layer is responsible for business logic, including transaction, account, and user-related activities. This layer contains the majority of the application logic.

-

Data Layer

The data layer is responsible for managing both structured and unstructured data, including databases such as PostgreSQL and MongoDB.

-

Integration Layer

FinTech applications require significant integrations with other systems, especially for banking and financial institutions. This layer is responsible for integrating with banks and other third-party applications, including financial data integrations.

-

Security Layer

Security is a crucial factor for FinTech applications, and this layer ensures the application is highly secure, with features such as authentication, authorization, and encryption.

-

API Gateway and Middleware

The API gateway connects all client requests to the application, making the application more efficient and manageable.

Modern FinTech Architecture Patterns

-

Monolithic vs Microservices

Traditional monolithic systems are easier to build initially, but become difficult to scale. Microservices architecture, on the other hand, breaks the system into smaller independent services, allowing teams to scale and update components independently.

-

Event-Driven Architecture

Event-driven systems use messaging queues to process real-time events such as transactions. This approach improves responsiveness and enables real-time financial operations.

-

Cloud-Native Architecture

Cloud platforms like AWS, Azure, and GCP provide the infrastructure needed for scalable and flexible systems. Cloud-native approaches support faster deployment, cost efficiency, and global accessibility.

-

API-First Architecture

APIs are the focal point in the system architecture in the FinTech domain. An API-first approach is important to ensure the seamless integration of external services, thereby supporting the implementation of functionalities such as payment gateway integration and open banking.

-

Modular Architecture

In the FinTech domain, the modern system architecture is designed to be modular, where components are easily replaceable without affecting the system as a whole, thereby supporting faster innovation and adaptability.

-

CAP Theorem in FinTech

In the context of distributed systems, the CAP theorem states the trade-off between consistency, availability, and partition tolerance, and the importance of balancing these parameters in the FinTech domain, especially in the case of real-time transactions.

Step-By-Step: How FinTech Software Is Built

-

Step 1: Define Product Scope and Use Case

The process begins with identifying the type of product being built, such as a digital wallet, lending platform, or neobank. Each use case has unique requirements that influence architecture decisions.

-

Step 2: Identify Regulatory Requirements

Compliance requirements are mapped early in the process. This ensures that the system design aligns with legal and regulatory standards from the start.

-

Step 3: Design System Architecture Blueprint

Architects create high-level diagrams that define system components, data flow, and integrations. This is the foundation of FinTech system architecture design.

-

Step 4: Evaluate Trade-offs and Constraints

Decisions are made based on factors such as cost, scalability, latency, and performance. This step ensures that the system is practical and sustainable.

-

Step 5: Choose the Technology Stack

Selecting the right tools and technologies is crucial. This includes frontend frameworks, backend languages, databases, and cloud infrastructure.

-

Step 6: Build Core Functional Modules

Core features such as authentication, transaction processing, and account management are developed. These modules form the backbone of the system.

-

Step 7: Implement API and Integration Layer

External integrations are added, including banking APIs, payment processors, and third-party services. This step is essential for building a complete FinTech platform architecture.

-

Step 8: Integrate Third-Party Services

Services such as identity verification, fraud detection, and analytics are integrated to enhance system capabilities.

-

Step 9: Implement Security Framework

Security measures such as OAuth, multi-factor authentication, and encryption are implemented across the system.

-

Step 10: Testing and Compliance Validation

The system undergoes rigorous testing, including security audits and compliance checks, to ensure reliability and safety.

-

Step 11: Deployment and Monitoring

The application is deployed using CI/CD pipelines, and monitoring tools are set up to track performance and detect issues in real time.

Technology Stack Used in FinTech Architecture

The choice of technology stack depends on the product’s requirements, scale, and compliance needs.

- Frontend Technologies

- React, Angular, Flutter

- Backend Technologies

- Node.js, Java, .NET

- Databases

- PostgreSQL, MongoDB, Redis

- Infrastructure

- Docker, Kubernetes

- Real-Time Processing

- Kafka, Spark

Selecting the right stack is a key part of FinTech software development, as it directly impacts performance, scalability, and maintainability.

Security Architecture in FinTech Systems

Security in FinTech is not limited to a single layer. It is integrated across the entire system.

Key elements include:

- Zero-trust architecture

- Data encryption in transit and at rest

- Identity and access management

- Fraud detection using advanced analytics

Continuous monitoring and audit systems ensure that threats are detected and mitigated in real time. Many platforms also leverage AI integration services to enhance fraud detection and risk analysis.

Scalability and Performance Considerations

FinTech systems must be designed to handle growth without compromising performance.

Key considerations include:

- Horizontal scaling to handle increased load

- Load balancing to distribute traffic efficiently

- Latency optimization for faster transactions

A well-designed, scalable FinTech architecture ensures that systems can support millions of users while maintaining consistent performance.

Quick Stat:

According to the World Economic Forum, FinTech companies report an average of 37% customer growth globally, reinforcing the need for systems that can scale efficiently and handle increasing user demand.

Challenges in Building FinTech Architecture

Several challenges are involved in the development of FinTech architecture, and they are:

- Dealing with complex and intricate regulatory issues

- Integration with the existing banking infrastructure

- Dealing with the need for real-time data processing

- Security

In addition, the cost, scalability, and performance factor is always an issue, and this is where the expertise in financial software development services becomes important, as they can develop the system effectively.

Quick Stat:

According to KPMG, global FinTech investment reached $116 billion in 2025, reflecting continued investor confidence in digital financial innovation and the growing demand for strong, future-ready platforms.

Future Trends in FinTech Architecture

The FinTech landscape is evolving rapidly, driven by technological advancements and changing user expectations.

Key trends include:

- AI-powered financial systems: AI is reshaping fintech by enabling smarter risk analysis, fraud detection, and personalized financial services. It helps platforms automate decision-making, improve accuracy, and deliver faster, data-driven user experiences at scale.

- Blockchain and decentralized finance: Blockchain and DeFi are transforming financial systems by removing intermediaries and increasing transparency. These technologies enable secure peer-to-peer transactions, smart contracts, and decentralized platforms that offer more control and trust to users.

- Embedded finance solutions: Embedded finance integrates financial services directly into non-financial platforms, allowing businesses to offer payments, lending, or insurance within their apps. This improves user convenience and creates new revenue opportunities across digital ecosystems.

- Serverless architecture: Serverless architecture allows fintech platforms to run applications without managing infrastructure, improving scalability and cost efficiency. It enables faster deployment, automatic scaling, and better handling of unpredictable transaction loads in modern financial systems.

These innovations are reshaping how FinTech app development is approached, enabling more efficient and intelligent systems.

Quick Stat:

According to the World Economic Forum, FinTech firms report 40% revenue growth and 39% profit growth, showing that the sector is moving beyond rapid expansion toward more sustainable and well-structured growth.

Conclusion

FinTech architecture is more than a technical foundation. It shapes how financial products perform, scale, integrate, and stay secure in a highly regulated environment. From defining system layers and selecting the right architectural patterns to supporting real-time transactions and compliance, every architectural decision directly impacts long-term product success.

As FinTech continues to evolve, businesses need systems that are not only reliable today but also flexible enough to support future growth, new integrations, and changing user expectations. A strong architectural approach helps reduce risk, improve performance, and create better digital financial experiences.

At EvinceDev, we help businesses build high-performing FinTech solutions with a focus on scalability, security, and seamless system design. Our expertise in FinTech software development spans from product planning and architectural strategy to custom platform development, integrations, and modernization for evolving financial ecosystems. For businesses looking to build or scale fintech products with confidence, the right architecture and the right development partner can make all the difference.