Money has continuously evolved alongside technological progress. From physical coins and paper notes to online banking and mobile wallets, each transformation has reshaped how value is exchanged. Today, we are witnessing the next major shift: the rise of government-backed digital money.

The financial world is rapidly moving toward digital transformation, and central bank digital currency initiatives are becoming a key part of this shift, creating new opportunities for fintech software development across payments, compliance, and digital banking infrastructure.

Unlike cryptocurrencies that operate outside government control, a central bank digital currency is regulated by a country’s central bank. As global economies digitize, these frameworks are being tested across multiple regions, signaling a potential transformation in how money moves internationally.

This blog explores what CBDCs are, why governments are accelerating their development, how they could impact banking and cross-border finance, and what their rise means for businesses, institutions, and the future of the global economy.

Quick Stat:

PwC’s Global CBDC Index shows that major economies such as India and China are among the most advanced in CBDC development, with large-scale pilots and near-live implementations already underway.

What Is a Central Bank Digital Currency (CBDC)?

A central bank digital currency is a government-issued digital form of national currency that operates on digital infrastructure and is backed by a central bank. It holds the same significance as traditional fiat money but exists entirely in electronic form.

In simple terms, a CBDC allows individuals and businesses to store and transfer money digitally while still using a currency controlled by the central bank.

Key characteristics of a CBDC

- Issued and regulated by a country’s central bank

- Represents legal tender just like physical cash

- Stored in digital wallets or authorized financial platforms

- Designed to improve payment efficiency and financial inclusion

Unlike decentralized cryptocurrencies, central banking digital currencies are subject to regulatory oversight, allowing governments to track financial flows and help ensure stability in the monetary system.

How Is It Different From Other Forms of Money?

CBDCs are often confused with other digital financial tools, but the differences are significant:

- CBDCs vs Cryptocurrencies: Cryptocurrencies are decentralized and operate without a central authority. CBDCs are centrally issued and controlled, prioritizing stability and regulation.

- CBDCs vs Stablecoins: Stablecoins are issued by private companies and pegged to fiat currencies. CBDCs are direct liabilities of central banks and carry sovereign backing.

- CBDCs vs Digital Banking Software: Traditional digital banking involves deposits at commercial banks. CBDCs represent a direct claim on the central bank itself.

What Are the Types of CBDCs?

- Retail CBDC: Designed for everyday use by businesses and individuals.

- Wholesale CBDC: Used by financial institutions for settlements and large transactions.

Why Are Governments Exploring CBDCs?

Governments worldwide are accelerating research into central bank digital currency systems as digital payments replace cash and financial systems modernize.

Several economic and technological factors are driving this interest.

Key reasons behind global interest

- Declining use of physical cash: In many economies, digital payments have already overtaken cash usage. Governments need a public alternative to private payment systems.

- Competition from cryptocurrencies and stablecoins: The rise of private digital assets has challenged traditional monetary systems. Governments want to retain control over currency issuance.

- Financial inclusion: Millions of people remain unbanked. Digital systems can provide access to financial services through mobile devices.

- Improved payment efficiency: Existing payment systems, especially cross-border ones, are slow and expensive. CBDC payment infrastructure can reduce friction.

- Better monetary policy implementation: Digital systems allow more precise tracking and distribution of money, enabling faster economic interventions.

- Combating illicit financial activity: Increased traceability can help reduce money laundering, fraud, and tax evasion.

Quick Stat:

According to the Atlantic Council’s CBDC Tracker report, CBDCs now cover almost the entire global economy, with 137 countries and currency unions representing 98% of global GDP exploring them, showing that this is no longer an experimental trend but a system-level transformation of finance.

Who Is Leading the CBDC FinTech Race Globally?

CBDC development is happening at different speeds across the world, with each country pursuing its own strategy.

Major economies

- China (e-CNY)

China is one of the most advanced, with large-scale pilot programs and integration into existing payment apps. - India (e₹)

India has launched both retail and wholesale pilots, leveraging its strong digital payment ecosystem. - European Union (Digital Euro)

The EU is focusing on privacy, security, and complementing existing financial systems. - United States

The U.S. remains cautious, prioritizing research while supporting private-sector innovation.

Smaller economies

- Bahamas (Sand Dollar)

One of the first fully launched systems, focused on financial inclusion. - Nigeria (eNaira)

Designed to improve access to digital payments and reduce reliance on cash.

This diversity shows that there is no one-size-fits-all approach to CBDCs. Each country is tailoring its approach based on its economic priorities.

Market Insight:

According to the Bank for International Settlements, 85 of the 93 central banks surveyed in 2024, or 91%, were exploring a retail CBDC, a wholesale CBDC, or both, showing how actively central banks are engaged in research and development.

How Do CBDCs Work Behind the Scenes?

While the concept of digital money sounds simple, the underlying technology is complex and varies by country.

Core technological components

- Centralized vs distributed systems: Some systems rely on centralized databases, while others use distributed ledger technology.

- Role of blockchain: Not all CBDCs use blockchain. Many central banks prefer controlled systems for better scalability and governance.

- Digital wallets: Users access funds through wallets provided by banks or authorized platforms.

- Identity verification systems: Ensures compliance with necessary regulatory standards, including KYC.

- Offline functionality: Being developed to ensure usability in areas with limited internet access.

These systems rely heavily on advanced fintech software to ensure scalability, security, and seamless transaction processing across digital financial networks.

What Are the Key Benefits of CBDCs?

CBDCs offer several advantages that could significantly improve financial systems.

Major benefits include:

- CBDC cross-border payments: Transactions can be processed almost instantly, even across borders.

- Lower transaction costs: Reduced reliance on intermediaries lowers fees.

- Greater transparency: Digital tracking reduces fraud and improves accountability.

- Financial inclusion: Expands access to financial services for underserved populations.

- Real-time settlement: Reduces delays and improves liquidity.

- Programmability: Enables innovative use cases such as automated financial flows.

To enable these capabilities, organizations are increasingly investing in fintech software development to build flexible and programmable financial ecosystems.

What Are the Risks and Challenges of CBDCs?

Despite their potential, CBDCs come with serious concerns that must be addressed.

Key challenges include:

- Privacy and surveillance concerns: Fully traceable systems could lead to increased government oversight of financial activity.

- Cybersecurity risks: National digital currency systems could become targets for cyberattacks.

- Impact on banks: If users move funds from banks to central bank wallets, traditional banking models could be disrupted.

- Adoption barriers: Public trust, digital literacy, and infrastructure gaps may slow adoption.

- Regulatory complexity: Designing policies that balance innovation with stability is challenging.

- Public trust issues: Without trust, even the most advanced system may fail to gain adoption.

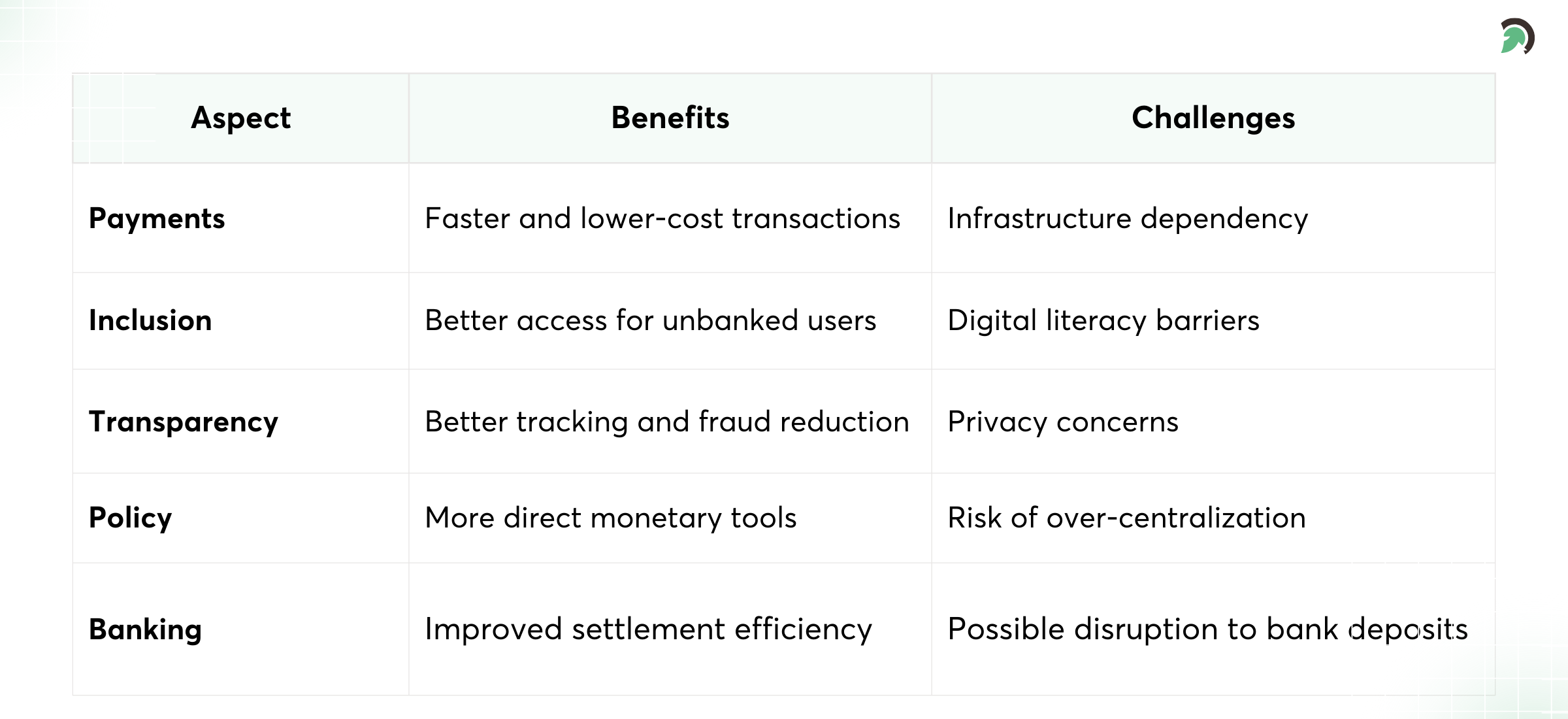

How Could CBDCs Impact Global Finance?

The emergence of central bank digital currency frameworks could fundamentally reshape global financial infrastructure.

-

Faster cross-border payments

Traditional international payments may take several days to settle. With interoperable systems, central banks could enable near-real-time international transactions. This could reduce costs for businesses engaged in global trade and supply chains.

-

New monetary policy tools

A centralised banking digital currency allows central banks to monitor money flows more precisely. Policymakers could implement stimulus programs more directly and efficiently.

-

Changes to banking structures

If consumers hold funds directly with central banks, commercial banks may face reduced deposits, leading to structural changes in the banking sector.

-

Increased transparency

Traceable systems enable better monitoring of financial activity, helping reduce fraud and illicit transactions.

This transformation will be driven by continuous innovation in fintech software, enabling faster, more transparent, and globally connected financial systems.

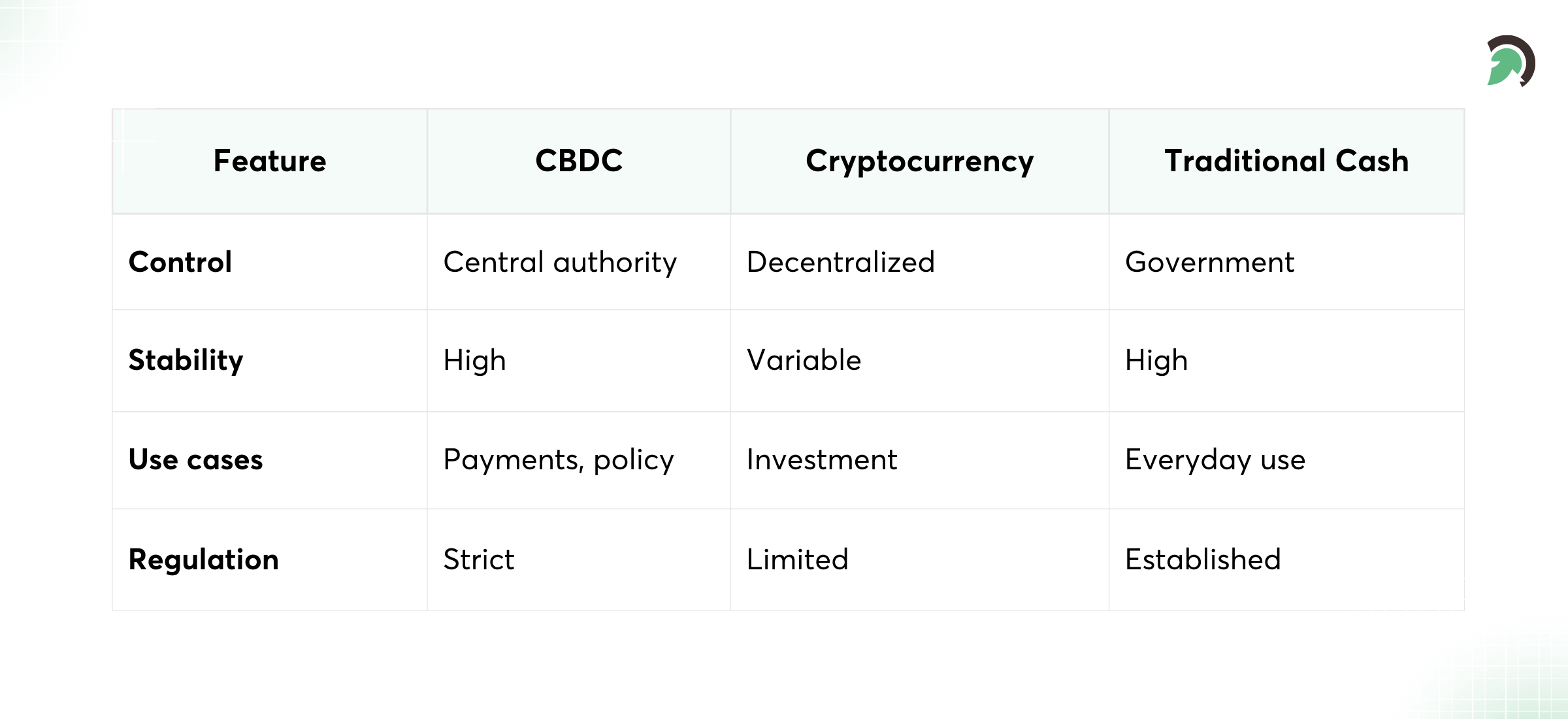

CBDCs vs Cryptocurrencies: Can They Coexist?

CBDCs and cryptocurrencies are often viewed as competitors, but their roles may be complementary.

Key differences

- Centralization vs decentralization

- Stability vs volatility

- Regulation vs open systems

CBDCs are designed for stability and compliance, while cryptocurrencies drive innovation and decentralization.

What Does the Future Look Like?

The most likely scenario is a hybrid ecosystem where:

- Governments manage regulated systems

- Private players innovate on top of them

- Users choose based on use case

Can CBDCs Improve Financial Inclusion in Emerging Markets?

CBDCs have strong potential to expand financial access, especially in developing economies.

Key opportunities

- Reaching unbanked populations through mobile devices

- Supporting mobile-first economies

- Enabling direct government transfers

- Reducing dependency on traditional banking infrastructure

India provides a strong example, where integration with existing systems like UPI could accelerate adoption and improve usability.

What Will Banking Look Like in a CBDC World?

CBDCs could reshape the role of banks rather than eliminate them.

Possible changes

- Reduced reliance on deposits

- Increased focus on financial services

- Greater collaboration with FinTech companies

- Expansion of digital wallet ecosystems

Banks may evolve from traditional intermediaries into service-driven financial platforms.

How Will Policy and Regulation Shape CBDCs?

The success of CBDCs depends heavily on policy design. As these frameworks evolve, financial institutions will also need stronger compliance automation solutions to manage reporting, identity verification, transaction monitoring, and regulatory oversight at scale.

Key considerations

- Balancing privacy and control

- Ensuring financial stability

- Creating interoperable global systems

- Developing regulatory frameworks

Institutions like the IMF and BIS are already working toward global coordination.

What Could the Next Decade of Digital Money Look Like?

Several possible scenarios could shape the future:

- Fully interoperable global systems

- Regional digital currency blocs

- Coexistence with crypto and stablecoins

- Slow adoption due to public concerns

The outcome will depend on technology, policy, and public acceptance.

Who Wins and Who Loses in a CBDC-Driven Financial System?

CBDCs introduce important questions about power and control.

- Governments gain greater visibility and control

- Consumers gain convenience but face trade-offs

- Banks may lose traditional advantages

Ultimately, design choices will determine the balance between public good and financial control.

CBDCs vs Stablecoins vs Traditional Money

To better understand how CBDCs compare with other forms of money, here is a simplified breakdown:

The future is likely to be a hybrid system where each form of money serves different purposes.

What Does This Mean for Businesses and Institutions?

For banks, enterprises, and startups entering this space, the opportunity extends beyond compliance and readiness into building fintech software development solutions that align with evolving market and regulatory expectations.

This shift will also create new opportunities for digital finance solutions that help institutions strengthen payment infrastructure, improve user experience, and enhance regulatory readiness.

Key implications

- Banks must rethink their business models

- FinTech firms can build new services

- Global companies benefit from faster transactions

- Payment providers must adapt

Early adopters will have a strategic advantage. As this ecosystem matures, organizations will need to rethink how they deliver CBDC financial services, from wallet experiences and transaction flows to security, governance, and user trust. In addition to product and infrastructure readiness, many organizations will benefit from financial technology consulting to identify practical use cases, assess risk, and align digital finance strategy with shifting market expectations.

Conclusion

CBDCs represent one of the most significant transformations in modern finance, with the potential to redefine how money is issued, transferred, and governed in a digital economy. Their promise lies in greater efficiency, broader financial inclusion, and new forms of innovation that could reshape both domestic and global financial systems.

At the same time, their rise brings equally important questions around privacy, control, interoperability, and financial stability. That is why the future of money will not be shaped by technology alone, but by the policy choices, infrastructure decisions, and trust frameworks built around it.

Rather than replacing every existing system, CBDCs are more likely to become part of a broader financial ecosystem where traditional banking, fintech innovation, and digital public infrastructure evolve together. For financial institutions, enterprises, and technology partners, this creates a clear need to prepare for a world where payment systems are smarter, more connected, and increasingly programmable.

As this shift accelerates, organizations will need the right strategy, infrastructure, and FinTech digital solutions to adapt to next-generation financial ecosystems. This is where experienced digital engineering and product teams, such as EvinceDev, can add value through fintech software development, helping businesses build secure, scalable, and future-ready solutions for an evolving financial landscape.

In the end, the real question is not whether digital money will become more influential. It is how effectively we design, regulate, and build around it.