Key Takeaways:

- Fintech APIs: Learn how fintech APIs connect apps, banks, and payment systems for seamless digital services.

- Payment Systems: Discover how payment API integration enables secure, fast, and real-time online transactions.

- Open Banking: Understand how open banking APIs securely share banking data across connected fintech apps.

- Lending APIs: Explore how APIs simplify loan approvals, credit scoring, and customer verification workflows.

- Fraud Security: See how API security in fintech helps detect fraud and protect sensitive financial data.

- Banking Connect: Learn how banking API integration improves account access, transfers, and financial services.

- API Best Tips: Explore fintech API integration best practices for security, scalability, and smooth performance.

- Future of APIs: Understand how APIs are shaping the future of fintech, digital banking, and embedded finance.

Think about the last time you made an online payment. You opened an app, entered the amount, tapped a button, and within seconds, the transaction was completed. From the user’s side, it feels simple and effortless.

Behind that smooth experience, however, the fintech app is communicating with multiple systems, including banks, payment gateways, security tools, and transaction processors. This communication is made possible through APIs.

API integration in fintech helps financial applications connect securely with different platforms and services. It enables payment apps, digital wallets, lending platforms, banking solutions, and investment apps to exchange data and process transactions in real time.

For fintech businesses, APIs make it easier to add payment features, verify users, detect fraud, access banking data, and launch new services without building everything from scratch.

In this blog, we’ll explore fintech API integration, its major use cases, benefits, challenges, and best practices in a simple and practical way.

Quick Stat:

According to McKinsey’s Global Payments Report 2024, digital payments continue to see strong global growth, driven by increasing adoption of real-time payments, digital wallets, and API-driven financial services across industries.

What Is API Integration in FinTech?

API stands for Application Programming Interface.

An API allows two different software systems to communicate and exchange information with each other. It works like a messenger that takes a request from one system, sends it to another system, and returns the response.

For example:

- A payment app uses APIs to connect with a bank and process transactions

- A loan platform uses APIs to check a customer’s credit score

- An investment app uses APIs to fetch live stock market data

- A digital wallet uses APIs to verify and confirm payments

- A fintech app uses APIs to complete KYC or identity verification

In the fintech industry, applications often need to connect with banks, payment gateways, credit bureaus, fraud detection tools, KYC providers, and other financial platforms. When these systems are connected through APIs, the process is called API integration in fintech.

API integration in fintech helps different financial systems work together securely and in real time. It acts as a bridge between fintech applications and the financial services they rely on.

Quick Stat:

According to Fortune Business Insights, the global fintech market was valued at USD 394.88 billion in 2025 and is projected to reach USD 1.76 trillion by 2034, highlighting the rapid growth of digital financial services worldwide.

Simple Example of API Integration in FinTech

Imagine you are shopping online and choose to pay through a digital payment app.

When you click “Pay Now,” the process may look instant from your side, but several systems start working together in the background.

Here’s what happens:

- The payment app sends your payment request

- The API carries this request to the payment gateway or bank

- The bank checks whether your account has enough balance

- The payment gateway processes and verifies the transaction

- The API sends the final response back to the app

- You receive a payment success or failure notification

All of this happens within a few seconds with the help of fintech APIs.

Without API integration in fintech, these steps would take much longer and may require manual coordination between banks, payment providers, and merchants. APIs make the entire process faster, more connected, and easier for users.

Why API Integration Matters in the FinTech Industry

Modern financial services rely heavily on speed, automation, security, and user convenience. Customers no longer want to wait several days for transactions to process or visit physical bank branches for basic financial tasks. They expect instant access to services through mobile apps and online platforms. This growing demand has made API integration in fintech more important than ever before. APIs help fintech businesses provide these experiences efficiently.

Traditional banking systems often worked in isolated environments. Integrating new services used to take months or even years. However, fintech API integration has made financial services much faster and more flexible.

Today, businesses use fintech APIs to:

- Process online payments

- Verify customer identities

- Access banking data

- Detect fraud

- Automate compliance

- Enable digital lending

- Offer investment services

For example, a fintech lending platform may use:

- Banking API integration for account verification

- Payment API integration for loan disbursement

- Credit bureau APIs for scoring

- Compliance APIs for KYC verification

Instead of building every feature internally, companies can integrate specialized APIs and launch products much faster.

This is why API integration in fintech has become one of the biggest drivers of innovation in the financial sector.

How API Integration Works in FinTech

The process behind API integration in fintech is easier to understand than many people think. APIs work quietly in the background, helping applications exchange information quickly and securely. Although the technology may sound technical at first, the actual workflow is quite simple when broken down step by step.

Step 1: User Sends a Request

A user performs an action such as:

- Making a payment

- Checking account balance

- Applying for a loan

- Transferring funds

Example:

A customer clicks “Send Money” in a mobile banking app.

Step 2: API Connects the App With the Service Provider

The application sends the request through an API to:

- A bank

- A payment gateway

- A fraud detection system

- A verification provider

This is where fintech API integration helps different systems communicate.

Step 3: The Provider Processes the Request

The provider verifies:

- User credentials

- Account balance

- Security checks

- Compliance requirements

For example, during payment API integration, the bank checks whether the user has enough balance.

Step 4: API Sends Back the Response

The provider sends the result back through the API.

Example:

“Transaction Successful”

Step 5: User Receives the Final Result

The user instantly sees the confirmation on the application.

This entire process usually takes only a few seconds because of financial API integration.

Types of APIs Used in FinTech

Different types of fintech APIs are used for different business needs. Some APIs connect internal systems, while others help fintech platforms communicate with banks, payment gateways, compliance tools, or third-party service providers. Choosing the right type of API is important because it affects performance, security, scalability, and user experience.

Internal APIs

- What it means: Internal APIs are used within an organization to connect its own systems and applications.

- Where it is used: Banks and fintech companies use them to connect mobile apps, customer databases, transaction systems, and internal dashboards.

- Example: A bank uses an internal API to connect its mobile banking app with customer account records.

- Benefit: It improves internal efficiency and allows secure data sharing between different systems.

Partner APIs

- What it means: Partner APIs are shared with selected and approved business partners.

- Where it is used: They are commonly used for integrations between fintech platforms, merchants, banks, payment gateways, and service providers.

- Example: A payment gateway provides partner APIs to ecommerce companies so they can accept online payments.

- Benefit: It helps businesses build trusted and controlled integrations with selected partners.

Open APIs

- What it means: Open APIs are available to external developers or third-party applications under defined rules and security standards.

- Where it is used: In fintech, open banking APIs are used to securely share banking data with customer consent.

- Example: A personal finance app uses open banking APIs to show balances from multiple bank accounts in one dashboard.

- Benefit: It improves financial transparency and gives users better control over their financial data.

Third-Party APIs

- What it means: Third-party APIs are provided by external service providers.

- Where it is used: Fintech companies use them for payments, fraud detection, credit scoring, KYC verification, analytics, notifications, and currency conversion.

- Example: A lending platform uses a third-party API to verify customer identity and check credit scores.

- Benefit: It reduces development time and helps fintech companies launch features faster.

REST APIs

- What it means: REST APIs are a common API style used to exchange data between systems over the internet.

- Where it is used: They are used in mobile apps, web platforms, cloud-based fintech systems, and banking applications.

- Example: A fintech app uses a REST API to fetch transaction history or check payment status.

- Benefit: They are flexible, lightweight, scalable, and easy to implement.

Webhook APIs

- What it means: Webhook APIs send automatic updates when a specific event happens.

- Where it is used: They are used for payment confirmations, failed transaction alerts, subscription updates, KYC status updates, and fraud alerts.

- Example: A merchant receives an instant notification when a customer’s payment is successful.

- Benefit: They help fintech platforms provide real-time updates and respond quickly to important events.

Top Use Cases of API Integration in FinTech

1. Payment Gateway Integration

One of the most common examples of API integration in fintech is payment processing. Digital payments have become a core part of modern financial services, and APIs help ensure these transactions happen quickly, securely, and efficiently across different banking and payment networks.

Payment API integration allows businesses to:

- Accept online payments

- Process UPI transactions

- Enable wallet payments

- Manage recurring subscriptions

- Support cross-border payments

- Track payment status in real time

Example

Apps like:

- Google Pay

- PhonePe

- Paytm

use fintech APIs to process millions of transactions daily.

Without payment API integration, digital payments would not work efficiently.

Benefits

- Faster transactions

- Better customer experience

- Secure payment processing

- Real-time payment tracking

2. Open Banking API Integration

Open banking APIs are transforming how financial data is shared between banks and third-party applications. Instead of keeping customer banking data locked within individual banking systems, open banking enables secure and permission-based data sharing that improves transparency and financial accessibility.

These APIs allow third-party applications to access banking information securely after customer approval.

Businesses use open banking APIs for:

- Account aggregation

- Transaction history access

- Bank account verification

- Personal finance management

- Payment initiation

Example

A budgeting app can connect with multiple bank accounts and display all balances in one place using banking API integration.

This improves convenience for customers and creates better financial visibility.

Quick Stat:

According to Open Banking Limited, the UK open banking ecosystem crossed 2 billion API calls in a single month, with more than 15 million users actively using open banking services.

3. KYC and Identity Verification APIs

KYC is an essential part of financial services.

FinTech companies use APIs to automate:

- Aadhaar verification

- PAN verification

- Document verification

- Face authentication

- AML screening

- Compliance checks

Example

When users sign up for a digital wallet, APIs instantly verify their identity documents. This reduces manual work and speeds up onboarding.

4. Fraud Detection and Risk Management APIs

Security is a major concern in the financial industry because financial platforms handle highly sensitive customer data and transactions every day. Even a small security issue can lead to fraud, financial losses, and reputational damage. This is why fintech companies invest heavily in fraud detection and risk management APIs.

FinTech APIs help businesses:

- Detect suspicious activity

- Monitor transactions in real time

- Generate fraud alerts

- Perform device fingerprinting

- Calculate risk scores

Example

If a user suddenly attempts a high-value transaction from another country, the fraud detection system can flag the activity immediately. Strong API security in fintech is essential for protecting customer information and preventing financial fraud.

5. Lending and Credit Scoring APIs

Loan providers use fintech API integration to automate loan approval processes.

These APIs support:

- Credit bureau integration

- Income verification

- Alternative credit scoring

- Loan eligibility checks

- Automated approvals

Example

Many instant loan applications approve loans within minutes because APIs automatically analyze customer data.

This improves efficiency and customer experience.

6. Banking and Core Financial System Integration

Banking API integration allows fintech platforms to connect directly with banking systems.

These APIs support:

- Balance inquiries

- Fund transfers

- Statement generation

- Card issuing

- Banking-as-a-Service integrations

Example

Neo-banking applications use financial API integration to provide banking features without becoming traditional banks themselves.

7. Accounting and ERP Integration

FinTech platforms often integrate with accounting systems to automate business operations.

These APIs help with:

- Automated reconciliation

- Invoice syncing

- Expense management

- Financial reporting

- Tax workflows

Example

Payment systems can automatically sync transaction records with accounting software. This reduces manual bookkeeping work.

8. Investment and Wealth Management APIs

Investment platforms use fintech APIs to provide trading and wealth management services.

These APIs support:

- Portfolio tracking

- Market data integration

- Trading execution

- Robo-advisory services

- Risk profiling

Example

Apps like Zerodha and Groww use API integration in fintech to display real-time stock market data and process investment transactions.

9. RegTech and Compliance API Integration

Compliance is a major part of financial services.

RegTech APIs help businesses:

- Perform AML checks

- Conduct sanctions screening

- Generate regulatory reports

- Maintain audit trails

- Manage customer consent

Example

Banks use compliance APIs to monitor suspicious transactions and meet regulatory requirements automatically.

This is another important area where API integration in fintech improves operational efficiency.

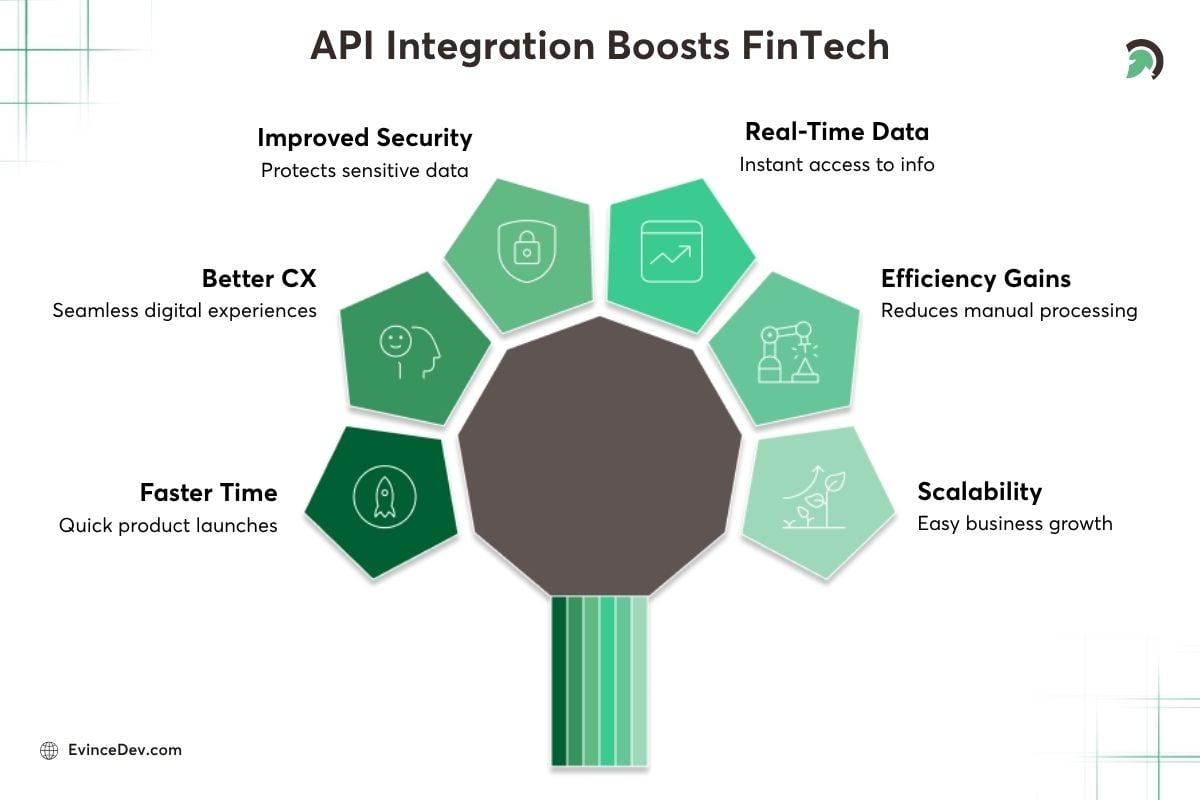

Key Benefits of API Integration in FinTech

Faster Time to Market

Businesses can quickly launch new products using existing fintech APIs instead of building every feature from scratch. For example, startups can integrate payment systems, KYC verification, and banking services rapidly using API development services.

Better Customer Experience

Customers expect seamless digital experiences.

FinTech API integration helps businesses offer:

- Instant onboarding

- Quick payments

- Real-time notifications

- Smooth account management

Improved Security and Compliance

Modern financial API integration includes:

- Encryption

- Authentication

- Secure token access

- Fraud monitoring

- Compliance workflows

Strong API security in fintech helps protect sensitive financial data.

Real-Time Data Access

FinTech APIs provide instant access to:

- Account balances

- Transaction history

- Market prices

- Payment status updates

This improves transparency and customer satisfaction.

Operational Efficiency

Automation reduces:

- Manual processing

- Human errors

- Administrative workload

- Processing delays

Scalability

API integration in fintech allows businesses to scale easily by adding new integrations and services as customer demand grows.

Common Challenges in FinTech API Integration

Although fintech API integration offers many advantages, businesses also face several challenges during implementation and long-term management. Integrating financial systems requires careful planning, strong security practices, and ongoing monitoring to ensure smooth performance.

Security Risks

Financial platforms are common targets for cyberattacks.

Weak API security can result in:

- Data breaches

- Fraud

- Unauthorized access

- Financial losses

This is why API security in fintech must always be prioritized.

Regulatory Complexity

FinTech businesses must comply with regulations such as:

- PCI DSS

- GDPR

- AML

- KYC

- PSD2

Managing compliance across multiple regions can become challenging.

Legacy Banking Systems

Many traditional banks still rely on outdated infrastructure. Integrating modern fintech APIs with older systems can be technically difficult.

Downtime and Reliability Issues

If a third-party API experiences downtime, financial services may be disrupted. For example, payment failures can negatively affect customer trust.

Integration Complexity

Managing multiple providers, systems, and APIs can become complicated as fintech platforms grow.

Best Practices for Successful FinTech API Integration

1. Choose Reliable API Providers

Select providers with strong uptime, security standards, clear documentation, compliance support, and scalable infrastructure. A reliable provider helps reduce downtime and keeps financial services running smoothly.

2. Prioritize API Security

Use strong authentication, encryption, token-based access, rate limiting, and secure data storage. Since fintech platforms handle sensitive financial data, API security in fintech should always be a top priority.

3. Follow Compliance Requirements

Make sure your fintech API integration follows relevant regulations such as PCI DSS, GDPR, PSD2, AML, KYC, and local financial rules. This helps reduce legal risks and build customer trust.

4. Use Sandbox Testing Before Production

Test APIs in a safe environment before going live. Check payment flows, failed transactions, webhooks, edge cases, and API errors to avoid issues after launch.

5. Build Proper Error Handling

Prepare your system for failed payments, duplicate transactions, timeout errors, and service outages. Good error handling improves reliability and gives users a smoother experience.

6. Monitor API Performance Continuously

Track uptime, latency, failed requests, transaction errors, and security alerts. Continuous monitoring helps identify problems early and maintain stable performance.

7. Plan for API Versioning

API providers may update or change their systems over time. Versioning helps prevent broken features and ensures your fintech platform continues working smoothly.

8. Design for Scalability

Build an API architecture that can handle growing users, higher transaction volumes, new integrations, and additional financial services as your business expands.

API Integration in FinTech: Real-World Examples

PayPal

PayPal uses payment API integration to support:

- Merchant payments

- International transfers

- Subscription billing

- Digital wallets

Stripe

Stripe provides fintech APIs that businesses use for:

- Payment processing

- Subscription management

- Fraud prevention

- Financial reporting

Plaid

Plaid is widely used for open banking APIs.

It helps applications:

- Connect with bank accounts

- Access financial data

- Verify accounts

- Analyze transactions

Razorpay

Razorpay supports:

- UPI transactions

- Banking API integration

- Subscription billing

- Online payments

- Merchant payment systems

How to Choose the Right FinTech API Integration Partner

Choosing the right partner is important for successful API integration in fintech. The right team can help you connect payment systems, banking platforms, KYC tools, fraud detection solutions, and compliance services without creating security or performance issues.

When evaluating a fintech API integration partner, businesses should look at:

- Security expertise: The partner should understand encryption, authentication, token-based access, and secure data handling.

- Compliance knowledge: They should be familiar with fintech regulations such as KYC, AML, PCI DSS, GDPR, and local financial guidelines.

- Scalability capabilities: The solution should support growing users, higher transaction volumes, and future integrations.

- API documentation: Clear documentation makes integration, testing, and maintenance easier.

- Technical support: Reliable support is important for fixing issues quickly and avoiding service disruptions.

- Industry experience: A partner with fintech experience will better understand payment flows, banking systems, and customer expectations.

Many businesses prefer working with companies that offer fintech custom software development and API development services. These services help fintech companies build secure, scalable, and customized platforms that match their business goals.

Future of API Integration in FinTech

The future of API integration in fintech looks extremely promising as financial services continue to become more digital, connected, and customer-centric. APIs are expected to play an even bigger role in enabling innovation across payments, banking, lending, insurance, and investment services.

Emerging trends include:

- AI-powered financial services

- Embedded finance

- Banking-as-a-Service

- Real-time payments

- Blockchain integrations

- Personalized banking experiences

- Advanced fraud detection

As digital finance continues to evolve, fintech APIs will become even more important in enabling seamless and intelligent financial services.

Businesses investing in fintech API integration today will be better prepared for future innovation and customer expectations.

Quick Stat:

According to Juniper Research, the number of global open banking users is expected to grow from 183 million in 2025 to more than 645 million by 2029, driven by increasing demand for digital banking and embedded finance services.

Conclusion

API integration in fintech is now essential for building fast, secure, and connected financial platforms. From digital payments and open banking to lending, fraud detection, and compliance, APIs help fintech businesses deliver smoother experiences while reducing manual work and improving operational efficiency. As customer expectations and regulatory demands continue to grow, businesses need scalable and secure integration strategies to stay competitive. This is where EvinceDev can support fintech companies with services like fintech custom software development and API development services. With the right technology partner, businesses can build reliable fintech solutions that connect systems efficiently, protect sensitive data, and support long-term growth.

Frequently Asked Questions (FAQs)

What is API integration in fintech?

API integration in fintech refers to connecting financial applications with banks, payment gateways, compliance systems, and third-party platforms using APIs.

Why are APIs important in fintech?

APIs help fintech companies automate financial services, process payments, access banking data, improve security, and deliver better customer experiences.

What are the most common fintech API use cases?

Common use cases include:

- Payment processing

- Open banking

- Loan approvals

- KYC verification

- Fraud detection

- Investment management

How do fintech APIs improve security?

Fintech APIs support encryption, authentication, fraud monitoring, and secure data sharing to protect financial information.

What are open banking APIs?

Open banking APIs allow third-party applications to securely access banking data with customer consent.

What challenges do businesses face during fintech API integration?

Challenges include:

- Security risks

- Compliance requirements

- Legacy banking systems

- Downtime issues

- Integration complexity

How do you choose the right fintech API provider?

Businesses should evaluate providers based on security, scalability, compliance support, documentation quality, and technical support.

Why should fintech companies work with an API integration partner?

Experienced partners offering fintech custom software development and API development services help businesses build secure, scalable, and compliant fintech solutions more efficiently.